Skip to comments.

How a mortgage clearinghouse became a villain in the foreclosure mess

The Washington Post ^

| 12/30/2010

| Ariana Eunjung Cha and Steven Mufson

Posted on 12/31/2010 7:13:49 AM PST by Chunga85

In the early 1990s, the biggest names in the mortgage industry hatched a plan for a new electronic clearinghouse that would transform the home loan business - and unlock billions of dollars of new investments and profits.

At the time, mortgage documents were moved almost exclusively by hand and mail, a throwback to an era in which people kept stock certificates, too. That made it hard for banks to buy and sell packages of home loans to investors. By contrast, a central electronic clearinghouse would allow the companies to transfer thousands of mortgages instantaneously, greasing the wheels of a system in which loans could be repeatedly and quickly bought and sold.

"Assignments are creatures of 17th-century real property law; they do not coexist easily with high-volume, late 20th-century secondary mortgage market transactions," Phyllis K. Slesinger, then senior director of investor relations for the Mortgage Bankers Association of America, wrote in paper explaining the system.

(Excerpt) Read more at washingtonpost.com ...

TOPICS: Business/Economy; Crime/Corruption; Government; News/Current Events

KEYWORDS: fannie; feddie; foreclosuregate; foreclosures; frank; freddie; homeownership; mers; mortgage; mortgages; pcloans; pcmortgages; politicallycorrect; scapegoat; title; villain

Lengthy but informative read...

1

posted on

12/31/2010 7:13:52 AM PST

by

Chunga85

To: frithguild; Lurker; FromLori; azhenfud; Wolfie; UCFRoadWarrior; servantoftheservant; ...

Read the comments section too..

Americans sure are happy *Ping*.

2

posted on

12/31/2010 7:15:59 AM PST

by

Chunga85

("Foreclosure Fraud", TARP, "Mortgage Crisis", Bailout)

To: Chunga85

MERS was driven by greed. First, they wanted a facility to bundle mortgages in to financial vehicles but the bankers could not do that unless they invented something like MERS. Second, the cheap SOB's wanted to circumvent paying local counties their due for handling the paperwork they have handled since the beginning of "time".

MERS was invented out of thin air. An analogy would be if google decided along with car lenders that google would create a database to handle the car liens while the states handled the actual title. This, of course, would not happen because it is so insane and the states would have fought it with their sizeable resources.

This may indeed bring the country down.

3

posted on

12/31/2010 7:40:33 AM PST

by

isthisnickcool

(Sharia? No thanks.)

To: Chunga85

A system set up by a Crook Angelo Mozillio (remember obama and dodd got friends of angelo home loans) now filled with toxic loans because of nothing but GREED that has cost taxpayers and investor’s/pension plans/401k’s Billions already imagine that from page two...

“Mozilo began brainstorming with a young MBA technology expert, Brian Hershkowitz, about ways to computerize and centralize the way the industry did business to take it to a new level.

“Angelo Mozilo loved to think about that,” Hershkowitz recalled. He was “the inspiration” for what would eventually become MERS.

In the fall of 1993, the MBA began circulating a white paper, “a blueprint for the future” that Hershkowitz wrote outlining a new central registry for mortgages.

Hershokwitz, who would later join Mozilo at Countrywide, modeled the new system on a clearinghouse for stocks called the Depository Trust Co. That company not only kept track of the stock ownership, it kept the physical certificates in a vault. Before the DTC had been created, brokers hired thousands of messengers to ferry certificates across New York City - a process that grew prohibitively expensive and inefficient as the volume of stock trades skyrocketed.

The mortgage industry was facing a similar problem. As interest rates sank, the number of new mortgages and refinancings soared. County recorders’ offices - which at that time were not automated - were having trouble keeping up.

Although the bankers touted the registry as a way to make mortgage processing more efficient, thus benefiting borrowers, they weren’t shy about admitting their main goal: more profits. They estimated that the cost of preparing, recording and mailing 11.1 million loan documents totaled about $210 million in the previous year alone.

In addition, the mortgage bankers had greater ambitions of hyper-charging the market for mortgage-backed securities. Invented in the late 1970s by a trader at Salomon Brothers, these investment packages pooled together thousands of mortgages. They were then sold not only to banks, but to pensions, insurance companies and other big investors.”

Not to mention that anyone who PAID them for this crappy service may have a great deal of trouble ever getting a clear title for their home.

4

posted on

12/31/2010 7:42:04 AM PST

by

FromLori

(FromLori)

To: Chunga85

“Comments” section seems to have disappeared.

5

posted on

12/31/2010 7:44:32 AM PST

by

DuncanWaring

(The Lord uses the good ones; the bad ones use the Lord.)

To: All

The impetus for a nationwide electronic database of mortgages originally came in the early 1990's from the biggest mortgage players - the MBA, Fannie Mae, Freddie Mac and Ginnie Mae .......... <><><> Fannie/Freddie are the key criminal mechanisms of the criminal enterprise that is the thieving Democrat party and its minions. <><><>

The Government filed suit against F/M head Franklin Raines when the depth of the F/M accounting scandal became clear. READ IT HERE http://housingdoom.com/2006/12/18/fannie-charges/

The Government noted, "The 101 charges reveal how the individuals improperly manipulated earnings to maximize their bonuses, while knowingly neglecting accounting systems and internal controls, misapplying over twenty accounting principles and misleading the regulator and the public. The Notice explains how they submitted six years of misleading and inaccurate accounting statements and inaccurate capital reports that enabled them to grow Fannie Mae in an unsafe and unsound manner."

These charges were made in 2006. The Court ordered Raines to return $50 Million Dollars he received in bonuses based on the mis-stated Fannie Mae profits. (Soon going to trial.) Freddie and Fannie, the two big quasi-govt mortgage banks that got a federal bailout used huge lobbying budgets and political contributions to keep regulators off their backs.

So which politicians get Fannie and Freddie political contributions. The top three U.S. Senators getting big Fannie and Freddie political bucks were Democrats and number two was then-Senator Barack Obama. who had only been in the Senate four years but still managed to grab the number two spot ahead of John Kerry, decades in the senate, and Chris Dodd then-chairman of the powerful Senate Banking Committee.

Fannie and Freddie were creations of the Congressional Democrats and the Clinton White House, designed to make mortgages available to more people, and as it turned out, some people who couldn’t afford them.

Fannie and Freddie have also been places for big Washington democrats to go to work in the semi-private sector and pocket millions.

The Clinton Administration’s White House budget director Franklin Raines was appointed by Clinton to run Fannie........ and collected $50 million dollars. Jamie Gurilli Gorelick (now BP's attorney), Clinton Justice Apartment Official, worked for Fannie and took home $26 million dollars.

Big Democrat Jim Johnson, recently on Obama’s VP search committee hauled in millions from his Fannie Mae CEO job. Now remember, Obama’s ads and stump speeches attacked McCain and Republican policies for the financial turmoil. It is demonstrably not Republican policy and worse, it appears the man attacking McCain, Senator Obama, was at the head of the line when the piggy’s lined up at the Fannie and Freddie trough for campaign bucks...." - FoxNews, Sept. 2008

McCain spoke forcefully on May 25, 2006, on behalf of the Federal Housing Enterprise Regulatory Reform Act of 2005: "Mr. President, this week Fannie Mae’s regulator reported that the company’s quarterly reports of profit growth over the past few years were “illusions deliberately and systematically created” by the company’s senior management, which resulted in a $10.6 billion accounting scandal.

The Office of Federal Housing Enterprise Oversight’s report goes on to say that Fannie Mae employees deliberately and intentionally manipulated financial reports to hit earnings targets in order to trigger bonuses for senior executives.

In the case of Franklin Raines, Fannie Mae’s former chief executive officer, OFHEO’s report shows that over half of Mr. Raines’ compensation for the 6 years through 2003 was directly tied to meeting earnings targets.

The report of financial misconduct at Fannie Mae echoes the deeply troubling $5 billion profit restatement at Freddie Mac.The OFHEO report also states that Fannie Mae used its political power to lobby Congress in an effort to interfere with the regulator’s examination of the company’s accounting problems. This report comes some weeks after Freddie Mac paid a record $3.8 million fine in a settlement with the Federal Election Commission and restated lobbying disclosure reports from 2004 to 2005. These are entities that have demonstrated over and over again that they are deeply in need of reform."

======================================

REFERENCE Franklin Raines,Clinton's appointee, looted and pillaged Fannie Mae. Raines famously bought into the climate control scam w/ F/M funds. Now he's hooked up with Ohaha's Chicago mob who organized the Chicago Climate Exchange.

================================================

REFERENCE Ex-Fannie CEO Franklin Raines should be behind bars for life. He is a crook of the first order. This thief Raines cooked the FM books precipitating losses of $9B (that we know of) for the single purpose of creating bonuses for himself and other F/M insiders. The SEC said Raines broke accounting rules by playing with risky derivatives.

RAINES COOKS THE F/M BOOKS---WALKS AWAY A MULTI-MILLIONAIRE After Raines was fired and exposed as a fraudster for cooking the govt books, Raines walked away w/ $90 million dollars, a $26 million parachute,

PLUS..... Raines gets a MONTHLY pension of $116,300 for life. Raines had already collected $4.87 million in special performance shares. Raines owns options giving him $5.8 million in net profit after redemptions, plus another $8.7 million in deferred compensation for six years at the F/M helm.

Raines keeps $5 million of paid-up life insurance. He and his spouse get free medical and dental benefits for life, worth over $1 million. Raines earned $20 million in salary, bonuses and stock awards (that we know of) in one year.

After he was fired, Raines told the F/M board that he's entitled to get paychecks until June 22 giving him another $600,000, which triggers a $2,000 monthly raise in his lifetime pension. He also said he's entitled to disputed options with a gross value of about $5.6 million. To keep Raines happy within philanthropic circles, Fannie Mae will match Raines' charitable contributions by $10,000 a year.

6

posted on

12/31/2010 8:01:01 AM PST

by

Liz

(There's a new definition of bipartisanship in Washington -- it's called "former member.")

To: All

REFERENCE----STATUS CUOMO-GILLIBRAND: Their fingerprints are all over the current depression/recession. Pass the word. When NY Gov-elect Cuomo was Housing and Urban Development Secy under Clinton, he was the prime mover behind programs that destabilized Freddie Mac and Fannie Mae, and his programs to mandate banks loan to low-income and bad-credit homebuyers were a significant factor in the housing collapse.

Congresswoman Gillibrand served as Special Counsel to Andrew Cuomo, Pres Clinton's appointee as Secy of HUD. Gillibrand played a key role in furthering HUD’s Labor Initiative and *New Markets initiative (sub-prime mortgages); Gillibrand worked to strengthen the Davis-Bacon Act and drafting new markets legislation for public and private investment in building infrastructure to revitalize lower income areas across the nation."

"Sure, I know how I got the HUD job. Clinton needed my daddy in his corner,

so I got the HUD job. HUD is where I got the $18 million to run for Governor."

CUOMO AND BILL CLINTON CREATED CONDITIONS FOR MELTDOWN (Village Voice 8-5-08) Andrew Cuomo, the youngest Housing and Urban Development secretary in history, made a series of decisions between 1997 and 2001 that gave birth to the country’s current crisis. He took actions that—in combination with many other factors—helped plunge Fannie and Freddie into the sub-prime markets without putting in place the means to monitor their increasingly risky investments. He turned the Federal Housing Administration mortgage program into a sweetheart lender with sky-high loan ceilings and no money down, and he legalized what a federal judge has branded “kickbacks” to brokers that have fueled the sale of overpriced and unsupportable loans.

Three to four million families are now facing foreclosure, and Cuomo is one of the reasons why.......

SOURCE http://www.villagevoice.com/2008-08-05/news/how-andrew-cuomo-gave-birth-to-the-crisis-at-fannie-mae-and-freddie-mac/

======================================

STATEMENT FROM NY GOVERNOR DAVID A. PATERSON

Appoints Kirsten Gillibrand to Hillary's Senate seat

FOR IMMEDIATE RELEASE: January 23, 2009

EXCERPT " During the administration of President Clinton, Congresswoman Gillibrand served as Special Counsel to Andrew Cuomo, Pres Clinton's appointee as U.S. Secretary of Housing and Urban Development." B> "At HUD, Congresswoman Gillibrand played a key role in furthering HUD’s Labor Initiative and *New Markets initiative, working to strengthen enforcement of the Davis-Bacon Act and drafting new markets legislation for public and private investment in building infrastructure to revitalize lower income areas across the nation." Following federal service, Congresswoman Gillibrand entered the private sector, joining one of the Country’s premier law firms.

READ MORE AT: http://www.state.ny.us/governor/press/press_0123091.html

7

posted on

12/31/2010 8:04:02 AM PST

by

Liz

(There's a new definition of bipartisanship in Washington -- it's called "former member.")

To: CutePuppy; ken5050; Condor51; stephenjohnbanker; TommyDale; martin_fierro; ...

Democrat Sen. Chris "Buy Me" Dodd is the best friend the lending industry's money can buy.....the poster child for ethical conflict ...... Dodd seems inclined to carve out sweetheart deals for himself and his pals, and then dissemble when his hand is found in the cookie jar.

“Mozilo began brainstorming with tech expert, Brian Hershkowitz, about

ways to computerize and centralize the way the mtge industry did business.

"Mozilo loved to think about that,” Hershkowitz recalled. He was “the

inspiration” for what would eventually become the discredited MERS.

Mozilo checks to make sure Sen Dodd is in his back pocket.

8

posted on

12/31/2010 8:16:06 AM PST

by

Liz

(There's a new definition of bipartisanship in Washington -- it's called "former member.")

To: DuncanWaring

Here's the link to the comments.

Comments

MERS scratched off all the VIN numbers on our houses for some reason.

This is a huge extremely complex mess and I think the bottom line will be a crushing transfer of not only wealth but private property.

9

posted on

12/31/2010 8:17:16 AM PST

by

Chunga85

("Foreclosure Fraud", TARP, "Mortgage Crisis", Bailout)

To: Liz

I went through 15 months of HELL with these MERS asshats in 06-07. That was all that was left on the mortgage, 15 stinking monthly payments and they did everything they could to make those payments *late*.

I was ready to .... 'explode'.

10

posted on

12/31/2010 10:05:22 AM PST

by

Condor51

(Suppose you were an idiot. And suppose you were a member of Congress. But I repeat myself.)

To: Liz; All

MERS is nothing more than a first electronic [records] exchange in what has been before a mess of manual / written records of mortgage "ownership" even when Fannie and Freddie had been in the business of purchasing and and then effective "securitization" of mortgages since Fannie's creation by FDR (to securitize for sale FHA loans).

Securitizing mortgages is not much different from "securitizing" partial "ownership" of "public" (in UK they call them "listed") companies on the stock exchanges - stocks give the owners of shares certain rights in proportion with their percentage of accumulated shares, or the corporate bonds which give their owners certain rights on the interest income as well as proportional "liens" on the assets of the company if it fails to pay such interest.

Neither stock shares' nor bonds' ownership gives the right to the "title" of the company or mortgage - it stays with the company or mortgagee, unless or until the company / title to the property is sold. It's almost a direct equivalent between fractional ownership of company stock / bond pool or mortgage - "title" ownership is not affected / changed / recorded until it's sold.

Essentially, MERS is a first electronic "mortgage exchange" in the same way NASDAQ was the first electronic stock exchange) - facilitating faster and better fractional "rights" to the flow of income (or loss) from particular asset class (mortgages, stocks, credit card interest etc.) and there were similar attempts to demonize / "discredit" the NASDAQ by its competitors NYSE and other exchanges because NASDAQ "didn't have people on the floor" who would catch "fat finger" and other mistakes that humans supposedly would take care of. Some 30+ years later and it's hard to find people on the "floor" of any sizable exchange because there are things that computers do much faster, better and more accurate, with fewer mistakes (e.g., databases and transaction processing).

MERS deals with real, already existing assets and market, not fictional, ephemeral, made up CO2 / carbon credits that CCX has been involved in.

It's not surprising that politicians who created the mortgage mess by requiring "politically correct" loans (CRA) from mortgage industry and executing the policy through FHA, VA and GSEs Fannie / Freddie, and their lap dogs in the al-media (WaPo and NYT et al) would find another "evil" organization responsible for all the problems and consequences of their own policies.

From New Ad Ties Barney Frank to Fannie & Freddie - FR, post #33 by CutePuppy:

Movie Review: Inside Job - Misdirected Outrage - B, by Gene Epstein, 2010 October 23 < snip > ..... In fact, contrary to the message of the film, securitization and the associated use of that now-anathematized investment instrument, derivatives, can be beneficial. For example, the activity of securitizing credit-card debt has been functioning for decades. Much depends on the underlying assets on which the derivatives and securities are based. When they are subprime mortgages, you just might have a problem.

Barney Frank has left a long trail as an aggressive supporter of the government-sponsored enterprises Fannie Mae and Freddie Mac, financial institutions that did not originate mortgages, but only bought them in the secondary market. The basic nature of the GSEs' business was therefore securitization, and increasingly of the subprime kind, which Frank extolled.

According to a front-page story in the Boston Globe, run the day before the Globe critic posted his rave of Inside Job, Congressman Frank actively opposed initiatives in 2003 and '04 to rein in Fannie and Freddie through tighter regulation ("Stance on Fannie and Freddie Dogs Frank," Oct. 14). "He and other House Democrats," reported the Globe, "also sent a letter to President George W. Bush in June 2004, saying the proposed crackdown could 'weaken affordable housing performance by emphasizing only safety and soundness.' ..... < snip >

MERS is not the "evil that lurks in the shadows" that unscrupulous politicians portray it trying to find any and every "problem" with "politically correct" mortgage fiasco that they can find, to diver attention from their role in it. It's actually a natural application of [computer] technology to the process of "securitization" - fractional ownership of assets - which provides the necessary liquidity to different potentially income-producing asset classes, and which has been done without being computerized long before that.

Happy New Year, everyone!

11

posted on

12/31/2010 11:22:32 AM PST

by

CutePuppy

(If you don't ask the right questions you may not get the right answers)

To: Chunga85

It’s just too bad. If the banks lose your paperwork then you get your deed to your house and land.

Too bad that greed drove the country to this but hey, we are only human.

Therefore of those running the new world order is to keep you enslaved.

12

posted on

12/31/2010 12:25:01 PM PST

by

ColdSteelTalon

(Light is fading to shadow, and casting its shroud over all we have known...)

To: CutePuppy

It's actually a natural application of [computer] technology to the process of "securitization" - fractional ownership of assets - which provides the necessary liquidity to different potentially income-producing asset classes, and which has been done without being computerized long before that. That was the intent, and it's all well and good if it was done right, but that doesn't appear to be the case. MERS was overwhelmed by the sheer number of transactions, in violation of many existing state recording laws, and provided support for robo-signed foreclosure affadavits that were inaccurate.

To: ColdSteelTalon

That is to say the goal of the those running the new world order is to keep you enslaved.

14

posted on

12/31/2010 12:27:07 PM PST

by

ColdSteelTalon

(Light is fading to shadow, and casting its shroud over all we have known...)

To: ColdSteelTalon; All

It’s just too bad. If the banks lose your paperwork then you get your deed to your house and land. These missing papers are not isolated incidents. There are many "reasons" why they are missing. And none of them are good.

Here's a woman who died in 1995 who continued her "robo-signing" until at least 2008.

Perfect..she's obviously unavailable for a deposition.

15

posted on

12/31/2010 12:31:56 PM PST

by

Chunga85

("Foreclosure Fraud", TARP, "Mortgage Crisis", Bailout)

To: Pearls Before Swine

MERS was overwhelmed by the sheer number of transactions... The answer is more technology, not less, and better quality of input - GIGO (Garbage In Garbage Out) - just as in any other database. The fact that this huge database can be run by less than 50 people, and that the number of actual, real mistakes to date (no doubt, coming from some county registrars input) in a 67 million entries has been insignificant, speaks very well of the program which provides general and national transparency to the mortgage records. There have been probably more errors overall in "title" assignments before and without MERS.

Robo-signing was done at places of mortgage origination and/or financing, not at MERS, and the sheer volume of that in the bubbling hot market certainly could have caused problems, but it didn't deal at all with the issue of securitization, which is what "show me the title" protesters are claiming.

The politicians, responsible for the "politically correct" lending to people who couldn't afford mortgages and few "social justice" lawyers and judges decided to make a BIG national issue of some inevitable mistakes in the process by BIG BANKS and BIG WALL STREET firms and BIG MORTGAGE / SECURITIZATION industry (which is now 90% owned or controlled by the Feddie) and they have practically halted the foreclosures process which is necessary for clearing out and reselling housing inventories.

That doesn't surprise me nor should it surprise anyone else. Dems and other "social justice" shakedown artists are very good at taking a case or few isolated mistakes, blowing it out of proportion and making a federal case out of it. There have been mistakes and issues with real estate titles before MERS (that's why there is "title insurance" and companies serving that industry) - computerizing it can only help in making it more transparent, leading to fewer mistakes in the future - it's no different in any other industry or service.

"Social justice" politicians and lawyers are profiting from making housing problems even worse, but they are given free pass because they found another bogeyman to divert attention to - now the problem is the technology. No wonder they want to dismantle MERS - mistakes can be fixed but transparency is a killer to their shakedown racket.

16

posted on

12/31/2010 1:30:29 PM PST

by

CutePuppy

(If you don't ask the right questions you may not get the right answers)

To: CutePuppy

>>The answer is more technology,

Technology is only as effective as allowed by the will to use it - and in the case of Fraud prevention in the financial industry...

"We didn't truly know the dangers of the market, because it was a dark market," says Brooksley Born, the head of an obscure federal regulatory agency -- the Commodity Futures Trading Commission [CFTC] -- who not only warned of the potential for economic meltdown in the late 1990s, but also tried to convince the country's key economic powerbrokers to take actions that could have helped avert the crisis. "They were totally opposed to it," Born says. "That puzzled me. What was it that was in this market that had to be hidden?"

>> BIG MORTGAGE / SECURITIZATION industry (which is now 90% owned or controlled by the Freddie)

Where are you getting that number?

17

posted on

12/31/2010 4:55:49 PM PST

by

LomanBill

(Animals! The DemocRats blew up the windmill with an Acorn!)

To: LomanBill

>> BIG MORTGAGE / SECURITIZATION industry (which is now 90% owned or controlled by the Freddie)

Actually, I said the Feddie, which is colloquial for Fannie+Freddie+FHA+VA (i.e., owned or guaranteed by the Federal government, implicitly before placing GSEs FNM and FRE in conservatorship, explicitly now), not Frediie. I make my share of typos, but this was not one. Hope it makes a difference :-)

That's an interesting assertion... Where are you getting that number?

It's more of a fact than an assertion... You can check the Feddie's combined balance sheets relative to the size of the mortgage market. The number is everywhere and has been quoted by economists and financial experts in various serious financial publications.

From Housing policy must be set on sustainable basis - WaPo, by Hank Paulson, 2010 July 30

< snip > ..... a big part of which requires reforming and dramatically scaling back Fannie Mae and Freddie Mac, the two government-sponsored housing enterprises that brought our nation's financial system and our entire economy to the brink of collapse. A significant root cause of the crisis was the combined weight of government policies promoting homeownership; these are apparent in the housing GSEs, the Federal Housing Administration (FHA), the Federal Home Loan Banks... < snip >

..... The GSEs, now placed in conservatorship, and the FHA still provide a massive subsidy to our housing market, touching more than nine out of 10 new mortgages.

From Wikipedia - Fannie Mae :

The Federal National Mortgage Association (FNMA) (OTCBB: FNMA), commonly known as Fannie Mae, was founded in 1938 during the Great Depression as part of the New Deal, but was set up as a stockholder-owned corporation chartered by Congress in 1968 as a government-sponsored enterprise (GSE). The corporation's purpose is to expand the secondary mortgage market by securitizing mortgages in the form of mortgage-backed securities (MBS), allowing lenders to reinvest their assets into more lending and in effect increasing the number of lenders in the mortgage market by reducing the reliance on thrifts. ..... < snip > In order for Fannie Mae to provide its guarantee to mortgage-backed securities it issues, it sets the guidelines for the loans that it will accept for purchase, called "conforming" loans. Mortgages that don't meet the guidelines are called "nonconforming". Fannie Mae produced an automated underwriting system (AUS) tool called Desktop Underwriter (DU) which lenders can use to automatically determine if a loan is conforming; Fannie Mae followed this program up in 2004 with Custom DU, which allows lenders to set custom underwriting rules to handle nonconforming loans as well.[35] The secondary market for nonconforming loans includes jumbo loans, which are mortgages larger than the maximum mortgage that Fannie Mae and Freddie Mac will purchase. In early 2008, the decision was made to allow TBA (To-be-announced)-eligible mortgage-backed securities to include up to 10% "jumbo" mortgages. ..... < snip >

Add to this the pressure of CRA (Community Reinvestment Act) on lenders to make "politically correct" community loans to people who couldn't afford it, along with the Feddie's steadily lowered loan standards to make guarantees for these loans possible, and the activity from "community organizers" like Obama who sued banks like Citi to make more loans, backed up by DOJ and activist HUD (Andrew Cuomo was HUD Secretary) during Clinton administration and have pieces of the seeds of the disaster.

This was not an accident or the result of "unregulated capitalist greed," it was a predictable consequence of decades of "politically correct" government housing availability / mortgage policy.

You might want to read through the FR thread Who Would Finance Mortgages If Fannie, Freddie Disbanded? - CNBC / FR posted by CutePuppy, 2010 July 02.

In particular, the thread has links and discussion on why Canada and her banks avoided this particular mortgage disaster and housing crash (hint: Canada didn't have CRA and "ownership society" as national policy, while maintaining the same or higher home ownership rate).

18

posted on

12/31/2010 7:02:16 PM PST

by

CutePuppy

(If you don't ask the right questions you may not get the right answers)

To: CutePuppy

>>Who Would Finance Mortgages If Fannie, Freddie Disbanded?

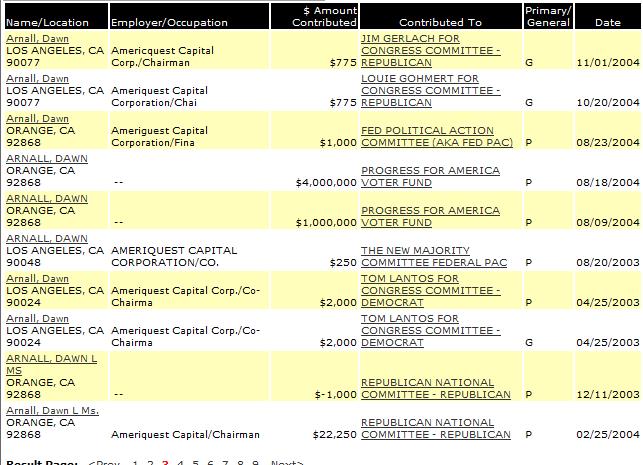

The same NyLon pipeline that predators like Ameriquest and Argent mortgage used to manufacture mortgage-backed A$$Paper?

19

posted on

12/31/2010 10:44:50 PM PST

by

LomanBill

(Animals! The DemocRats blew up the windmill with an Acorn!)

To: CutePuppy

>>The number is everywhere

Everywhere but here, evidently.

Why don't you parrot ~it for us, like you're parroting the "fiscally conservative" party line? And then, how 'bout you tell the class who this...

...is?

20

posted on

12/31/2010 10:56:18 PM PST

by

LomanBill

(Animals! The DemocRats blew up the windmill with an Acorn!)

Disclaimer:

Opinions posted on Free Republic are those of the individual

posters and do not necessarily represent the opinion of Free Republic or its

management. All materials posted herein are protected by copyright law and the

exemption for fair use of copyrighted works.

FreeRepublic.com is powered by software copyright 2000-2008 John Robinson