Skip to comments.

Atlantic Magazine Proclaims Ben Bernanke "THE HERO"

Townhall.com ^

| March 23, 2012

| Mike Shedlock

Posted on 03/23/2012 5:08:24 AM PDT by Kaslin

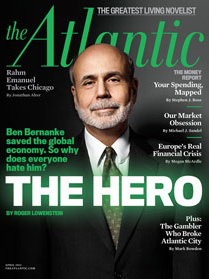

If you are looking for the most nauseating cover possible on Ben Bernanke, please consider the April 2012 issue of the Atlantic.

The cover asks the question "Ben Bernanke saved the global economy. So why does everyone hate him?"

For starters Ben Bernanke did not save the global economy. Making such a proclamation is like a football fans proclaiming victory at the end of the third quarter with the score 54-24 following a 24 point rally after being down 54-0.

Simply put, it is far too early to make a presumption the Fed "saved" anything given the global economy remains hugely imbalanced and highly vulnerable.

Furthermore, we can state without a doubt Bernanke is Inflationist Jackass, Devoid of Common Sense, and Clueless About Trade, Debt, History, and Gold.

Even if the game was over, why should any credit be given when we can say without a doubt the Fed caused the global economic crisis in the first place?

Once again I repeat ....

Bernanke: Why are we still listening to this guy?

The following video should make people think twice about listening to anything that Chairmen of the Fed Ben Bernanke says. It's a compilation of statements he made from 2005-2007 that will have your head spinning.

Please play that video. Bernanke proves over and over again he is a clueless jackass, devoid of common sense.

Proving that he cannot think clearly, Roger Lowenstein, writer for the Atlantic says "The visceral criticism of Bernanke is hard to fathom." Really?

Lowenstein concludes with "history may marvel that Bernanke has been a success".

Contrarian Cover Indicator

I suggest the cover for the Atlantic will prove to be as contrarian as the Time Magazine Home $weet Home | June 13, 2005 cover.

I used that cover to call a top in housing. Take that Atlantic cover as another huge contrarian indicator.

Given the enormous global imbalances that still remain were caused by the Fed, given that "too big to fail" has become "too bigger to fail", given that those on fixed income have been crucified by Fed policies, and given US deficits are over $1 trillion as far as the eye can see, the idea the "global economy has been saved" by the Fed is preposterous.

Jo Weisenthal writing for the Business Insider claims Ben Bernanke Just Murdered The Gold Standard.

In an equally feeble post, Simone Foxman also writing for the Business Insider writes Ben Bernanke Explains Why The World Will Never See Another Gold Standard.

What is the Proper Supply of Money?

Let's start with Simone Foxman who says

Bernanke pointed out various reasons that there's simply "not enough gold" to sustain today's global economy. First, extracting gold from the ground is a costly and uncertain endeavor. There is a limited amount of gold in the world, and it just doesn't make sense in the modern world for central or commercial banks store large amounts of gold in vaults. The size of the gold supply and inconvenience of the metal renders it too impractical to keep up with the pace of global commerce.

Startling Truth About Money Supply

Please consider a snip from a free eBook on Mises.Org by Murray Rothbard, What Has Government Done to Our Money?

An increase in the money supply, then, only dilutes the effectiveness of each gold ounce; on the other hand, a fall in the supply of money raises the power of each gold ounce to do its work. We come to the startling truth that it doesn’t matter what the supply of money is. Any supply will do as well as any other supply. The free market will simply adjust by changing the purchasing power, or effectiveness of the gold-unit. There is no need to tamper with the market in order to alter the money supply that it determines.

That snip is on page 29. Inquiring minds should start reading on page 26, the beginning of the chapter The “Proper” Supply of Money.

Moreover, I would like to point out that if there was a "proper" supply of money, different than stated above, the jackasses at the Fed (and the bubbles they have blown) have without a doubt proven they sure do not know what it is.

As Russia (and numerous other countries) have proven throughout history, the very idea that a bunch of central planners sitting in a room can decide on the proper supply of virtually anything is inane. Only free markets, operating without artificial interference from clueless bureaucrats can do that.

Price Volatility

Simone Foxman continues with still more economic drivel.

Second, while advocates of the gold standard are right that prices remain stable in the long-term, "on a year to year basis, that's not true." Limited supplies of gold—or changes to the supply of gold—cause prices of goods to be volatile in the short-term, regardless of long-term price stability.

Now that's pretty interesting. Simone admits that prices under a gold standard remain stable in the long term but she, like Bernanke is worried about the short-term.

There are two errors in in that short snip. Did you catch them? The first error is prices under a gold standard are not necessarily stable in and of themselves (short or long-term). Rather prices are relatively stable under a gold standard if and only if banks do not lend out more gold than there is.

History shows that alleged problems of the "gold standard" are primarily a problem of central bank interest rate manipulations in conjunction with fractional reserve lending that allows banks to lend out more money than there is gold backing it up.

The John Law Mississippi Bubble is a classic example.

Certainly when it comes to short-term price stability, the Fed does not have a leg to stand on. The housing bubble and its collapse and the dot-com bubble and its collapse are proof enough. How anyone could miss those analogies is nearly beyond belief, but Simone Foxman managed to do it.

Inability to Open Up Credit

Foxman continues with ...

[Bernanke] pointed to a substantial tome of economic research finding that the gold standard aggravated the Great Depression, saying "the gold standard was one of the main reasons the Great Depression was so bad and so long." The inability of the Federal Reserve to control monetary policy—open up credit, address unemployment, and drive business demand—left it with much less power to avert or mitigate the decade-long crisis. Bernanke added that countries not tied to the gold standard also had a much easier time getting out of the Depression. In the modern world, he said, "we've seen that problem with various kinds of fixed exchange rates."

Bernanke Says Pigs Can Fly

In other news, Bernanke said "pigs can fly" and Foxman concluded "pigs can fly". Seriously, just because someone in authority says something, does not make it true.

Proper analysis shows the true cause of the great depression was the enormous runup in credit and money the preceded it, just as happened in the Mississippi Bubble scheme. With that in mind, it is beyond silliness to propose more credit and more money is the cure for a problem caused by too much money and too much credit.

To believe so is to believe the solution to the Mississippi Bubble would have been to print still more money in the wake of that economic collapse.

Sorry Simone Foxman, You Can't Think Independently

Foxman concludes with "Sorry, Ron Paul. We think Bernanke just destroyed your position."

I conclude Foxman cannot think on her own accord, accepting economic drivel as fact because it comes from a position of authority.

Jo Weisenthal's Drivel

Let's now turn our attention to a point-by-point rebuttal of economic drivel presented by Jo Weisenthal.

Weisenthal: To have a gold standard, you have to go dig up gold in South Africa and put it in a basement in New York. It's nonsensical.

Mish: In my rebuttal to Simone Foxman, I stated that any amount of money was sufficient. One does not need to dig up more gold to have a proper supply. However given the credit bubble and the housing bubble, it should be quite clear we had vastly more supply of paper money than needed.

Weisenthal: The gold standard ends up linking everyone's currencies.

Mish: So what? Look what happened after Nixon closed the gold window. We have had nothing but problems, temporarily masked over by printing more money until things blew sky high, culminating in bank bailouts at taxpayer expense, and those on fixed income crucified in the wake.

Bear in mind, no one needs to fix the price of gold in dollars or any other currency. Indeed that is the wrong way to do it. Rather, one dollar should represent "x" amount of gold. As long as fractional reserve lending does not come into play and banks do not lend out more money than they have gold, problems under a gold standard would be far less than they are now. History suggests the same.

By the way, nothing about "linking" stops devaluations. For example, suppose the Drachma is defined as 1 drachma is redeemable for 1/1000th of an ounce of gold. Tomorrow, nothing stops the Greek government from saying, effective immediately you can only get 1/2000th of an ounce of gold for a drachma. That is a 50% devaluation, something Greece is unable to do now, on a "Euro standard".

Weisenthal: [A gold standard] creates deflation, as William Jennings Bryan noted. The meaning of the "cross of gold" speech: Because farmers had debts fixed in gold, loss of pricing power in commodities killed them.

Mish: Hello Joe. Please tell me how many in this country would not like to see lower prices at the gas pump, lower prices on food, lower rent prices, lower prices on clothes? The fact of the matter is price deflation is a good thing. The only reason why it seems otherwise is debt in deflation is harder to pay back. That is not a problem with deflation, that is a problem of banks foolishly lending more money than can possibly be paid back. Fractional reserve lending is the culprit.

Weisenthal: The economy was far more volatile under the gold standard (all the depressions and recessions back in the pre-Fed days).

Mish: Really? On what planet? Did the collapse in the housing bubble affect your ability to reason? Except for cases like Weimar, Mississippi Bubble, and for that matter all bubbles, gold provided stability. The bubbles (and the subsequent collapses) were caused by fractional reserve lending, not the gold standard.

Weisenthal: The only way the gold standard works is if people are convinced that the central bank ONLY cares about maintaining the gold standard. The moment there's a hint of another priority (like falling unemployment) it all falls apart.

Mish: That is one of the silliest defenses of paper money I have ever seen. The fact of the matter is, the ONLY reason paper money works at all is governments mandate its use. The free market would never except as money something that can be created at will in infinite supply. The idea that gold would "fall apart" in the case of employment conditions is simply inane.

Weisenthal: Gold standards leave central banks open to speculative runs, since they usually don't hold all the gold.

Mish: In a series of weaker and weaker arguments, Weisenthal proves 100% without a doubt he does not know a damn thing about either gold or what causes bank runs.

What Causes Bank Runs?

- Lending out more money than there is gold backing it up

- Duration mismatch - Banks secure money for 5 years via CDs then lend the money for 30 year mortgages. The problem comes when people want their money back after 5 years and it isn't there.

Both practices are fraudulent. They are the equivalent of selling the Brooklyn Bridge without having ownership of it.

Conclusion

All of the problems allegedly caused by the gold standard are in fact properly attributed to one of the following four things:

- Central banks and their inept Soviet-style central planning

- Fractional reserve lending

- Fed manipulation of interest rates

- Government sponsored monetary printing, frequently but not always to fight absurd wars that have no justified explanation. The War in Vietnam and the War in Iraq are recent examples.

The biggest housing bubble in history happened because the Greenspan Fed held interest rates too low too long. I made that case recently in a pair of related posts:

Here is the key chart and commentary from the first link.

HPI-CPI

click on chart for sharper image

The Fed kept interest rates at historic lows between 2002 and mid-2004. The last two rate cuts by Alan Greenspan were not justified at all, by any measure, and downright absurd considering the bubble brewing in housing prices vs. rent.

Certainly the Greenspan Fed ignored (cheerleaded is a better word), the housing bubble every step of the way. Bernanke defended the housing bubble and failed to see its consequences.

The most amazing, and galling thing, is Bernanke has the nerve to preach about "price stability" in the wake of that collapse.

In regards to trade, I ask you to read Hugo Salinas Price and Michael Pettis on the Trade Imbalance Dilemma; Gold's Honest Discipline Revisited

Finally it is important to point out it is those with first access to money that benefit from inflation. Who is that?

- Banks, because they can conjure up loans out of thin air and the Fed will bail them out if they go bust

- The already wealthy

- Government (via tax confiscation, especially property taxes)

By the time money is readily available to any fool who wants it, it is primarily fools who want it. Once again, the housing bubble is proof enough.

Those on fixed income and those in the middle class have been hammered by Fed policies. If you are looking for a reason for the shrinking middle class, then look at the Fed.

For some reason Jo Weisenthal and Simone Foxman are not only listening to Bernanke's economic drivel, they actually believe it and are attempting to spread the word.

TOPICS: Business/Economy; Editorial

KEYWORDS: fallingdollar; gasprices; georgesoros; hyperinflation; inflation; moneyprinting; weakdollar; weimar; weimarrepublic; zimbabwe

1

posted on

03/23/2012 5:08:27 AM PDT

by

Kaslin

To: Kaslin

One man's hero is another man's scum sucking, butt licking, over educated undercover Progressive.

2

posted on

03/23/2012 5:22:14 AM PDT

by

cashless

(Unlike Obama and his supporters, I'd rather be a TEA BAGGER than a TEA BAGGEE.)

To: Kaslin

Yeah, it's "fixed" all right.

3

posted on

03/23/2012 5:22:59 AM PDT

by

Travis McGee

(www.EnemiesForeignAndDomestic.com)

To: Kaslin

Very good article. Thanks for posting. DISMANTLE the FED. UNaccountable bureaucrats (socialists). See how they roll...

http://www.usdebtclock.org/

...over all of us.

DEPOPULATE socialists from the body politic.

DEFUND socialist collectives, foreign and domestic. (pick some...any of them...the 1st 100 you pick would be a good start)

live - free - republic

“Above all, if you wish to be strong, begin by rooting out every particle of socialism that may have crept into your legislation. This will be no light task.” - Frederic Bastiat 1801-1850

4

posted on

03/23/2012 5:23:48 AM PDT

by

PGalt

To: Kaslin

5

posted on

03/23/2012 5:30:27 AM PDT

by

Carriage Hill

(I'll "vote for an orange juice can", over Barry 0bummer and another 4yrs of his Regime From Hell!)

To: Kaslin; All

“The law is the organization of the natural right of lawful defense. It is the substitution of a common force for

individual forces. And this common force is to do only what the individual forces have a natural and lawful right to do:

protect persons, liberties, and properties; to maintain the right of each and to cause justice to reign over us all.”

—Frederic Bastiat

The quote from Bastiat AND HUGE CUTS proposed by a congressman...(37 pgs)

http://www.randpaul2010.com/wp-content/uploads/2011/01/Overview-500-billion-cuts-2.pdf

The cliff notes version...here...

http://washingtonexaminer.com/politics/beltway-confidential/2011/01/detailed-look-rand-paul-spending-bill/140043

HOORAY Rand Paul!

More Bastiat...

Now, legal plunder can be committed in an infinite number of ways. Thus we have an infinite number of plans for organizing it: tariffs, protection, benefits, subsidies, encouragements, progressive taxation, public schools, guaranteed jobs, guaranteed profits, minimum wages, a right to relief, a right to the tools of labor, free credit, and so on, and so on. All these plans as a whole — with their common aim of legal plunder — constitute socialism.

But how is this legal plunder to be identified? Quite simply. See if the law takes from some persons what belongs to them, and gives it to other persons to whom it does not belong. See if the law benefits one citizen at the expense of another by doing what the citizen himself cannot do without committing a crime.

6

posted on

03/23/2012 5:36:59 AM PDT

by

PGalt

To: Kaslin

One man's hero is another man's over educated, scum sucking, undercover Progressive son of a cur dog.

7

posted on

03/23/2012 5:57:12 AM PDT

by

cashless

(Unlike Obama and his supporters, I'd rather be a TEA BAGGER than a TEA BAGGEE.)

To: Kaslin

The articles in the atlantic are pointless, tasteless, ill-written, verbose, pompous, juvenile and pale in comparison to an 8 year old’s gushing love note.

8

posted on

03/23/2012 7:02:27 AM PDT

by

blueunicorn6

("A crack shot and a good dancer")

To: Kaslin

The Bureau of Labor Statistics is lying about the job numbers.

Supposedly, California added 18% of the new jobs in the US last year (283,200 out of 1,435,800). Meanwhile, their state personal income tax revenue was dropping a half a billion dollars. Neat trick, that:

CA: Add 250,000 Jobs, Lose .5 Billion in Revenue

The phony "Recovery" is just a ploy to get Obama re-elected. There is a moderate recovery happening in some of the smaller states around DC and in the southeast, and in the heartland. But the big states are sputtering.

9

posted on

03/23/2012 7:18:29 AM PDT

by

kiryandil

(turning Americans into felons, one obnoxious drunk at a time (Zero Tolerance!!!))

Disclaimer:

Opinions posted on Free Republic are those of the individual

posters and do not necessarily represent the opinion of Free Republic or its

management. All materials posted herein are protected by copyright law and the

exemption for fair use of copyrighted works.

FreeRepublic.com is powered by software copyright 2000-2008 John Robinson