Skip to comments.

Paulson Point Man on CDO Deal Emerges as Key Figure (Paolo Pellegrini)

WSJ on Yahoo ^

| 4/19/10

| Gregory Zuckerman

Posted on 04/19/2010 7:46:39 PM PDT by NormsRevenge

In 2004, Paolo Pellegrini was out of a job, living in a one-bedroom apartment in Westchester County, N.Y., with little money in the bank. He soon managed to land a gig working for hedge-fund manager John Paulson.

Today, after helping Paulson & Co. score $20 billion with a bet against housing and pocketing about $175 million for himself, Mr. Pellegrini is an unnamed but key character in the government's lawsuit against Goldman Sachs Group Inc. (NYSE: GS), according to people familiar with the matter.

The government alleges the bank deceived investors by selling them mortgage securities that the hedge fund had a hand in creating without disclosing the hedge fund's role in the deal or its bearish view on it. Mr. Pellegrini was Mr. Paulson's key representative on the deal, ..

Goldman denies it did anything wrong and is fighting the civil lawsuit filed Friday by the Securities and Exchange Commission in a New York federal court. Neither the hedge fund nor Mr. Pellegrini has been accused of wrongdoing.

The following account about Mr. Pellegrini is based on interviews with people familiar with him and his role at Paulson & Co. and the government's complaint.

Mr. Pellegrini, a stylish native of Italy, began his mostly disappointing Wall Street career in the mid-1980s. He had been a midlevel investment banker at Lazard Freres and tried a few other trading ventures. Two high-profile marriages—to Claire Goodman, daughter of legendary New York State senator Roy Goodman, and to Beth Rubin DeWoody, daughter of the late New York real-estate mogul Lewis Rudin—ended in divorce.

Then Mr. Paulson, an acquaintance, granted Mr. Pellegrini an interview in 2004. Some at the firm were reluctant to bring on Mr. Pellegrini, who lacked experience in some areas the hedge-fund did work in. Mr. Paulson hired him anyway ..

(Excerpt) Read more at finance.yahoo.com ...

TOPICS: Business/Economy; Crime/Corruption; Extended News; Government; US: New York

KEYWORDS: goldmansachs; johnpaulson; paolopellegrini; paulson; pellegrini; pointman

Navigation: use the links below to view more comments.

first 1-20, 21-25 next last

To: NormsRevenge

The government alleges the bank deceived investors by selling them mortgage securities that the hedge fund had a hand in creating without disclosing the hedge fund's role in the deal So when Barney Fwank, Dodd and Cuomo forced banks to make bad loans and then assured the public over and over again that everything was peachy keen that's supposed to be different?

2

posted on

04/19/2010 7:50:37 PM PDT

by

what's up

To: NormsRevenge

” In 2004, Paolo Pellegrini was out of a job, living in a one-bedroom apartment in Westchester County, N.Y., with little money in the bank. He soon managed to land a gig working for hedge-fund manager John Paulson.”

” In early 2006 Mr. Paulson asked him to size up whether housing was in a bubble. After weeks of work, Mr. Pellegrini came back with historical data suggesting homes were very overpriced. He then helped Mr. Paulson figure out how to place a wager on that view. They decided to bet against subprime mortgages through insurance-like contracts that rise in value if the bond declines in value or defaults.

Messrs. Paulson and Pellegrini turned to Wall Street to ask various firms to create pools of debt, known as collateralized debt obligations, backed by subprime mortgages so that the Paulson team could buy this insurance protection on them.”

“For Mr. Pellegrini, 53-years-old, who now runs his own hedge fund after leaving Paulson just over a year ago, the trade has worked out well.

In late 2007, he took his new wife on vacation in Anguilla, an island in the West Indies. Stopping at a cash machine in the hotel lobby to withdraw some cash, she checked the balance of their checking account. On the screen was a figure that startled her: $45 million, newly deposited in their joint account. It was part of Mr. Pellegrini’s $175 million bonus that year.”

“

3

posted on

04/19/2010 7:50:46 PM PDT

by

Pelham

(Obamacare, the new Final Solution.)

To: NormsRevenge

there are laws on the books to handle these cases.

we don’t need more!!

4

posted on

04/19/2010 7:59:16 PM PDT

by

elpadre

(AfganistaMr Obama said the goal was to "disrupt, dismantle and defeat al-Qaeda" and its allies.)

To: what's up

“So when Barney Fwank, Dodd and Cuomo forced banks to make bad loans”

You might want to check your facts. You are confusing CRA regulated depository banks with Wall Street investment banks. This concerns investment banks, not commercial banks. Wall Street investment banks weren’t subject to regulations forcing them to make loans.

Not only weren’t they forced to make subprime loans, they actively sought to get laws changed to let them get into that market. They were cranking out trillions of dollars of risky paper because it made them incredible amounts of money.

5

posted on

04/19/2010 8:00:01 PM PDT

by

Pelham

(Obamacare, the new Final Solution.)

To: elpadre

“there are laws on the books to handle these cases.”

You may be surprised. Goldman Sachs had officials in the last three administrations and they didn’t ignore the interests of their own industry. This SEC action is a civil action, not criminal. Crime pays, especially if you have the juice to insure that laws get changed to protect you.

6

posted on

04/19/2010 8:04:24 PM PDT

by

Pelham

(Obamacare, the new Final Solution.)

To: Pelham

I worked for the former GMAC Commercial Mortgage in the run up years to them being sold OFF to help keep GM afloat. They were bought by Capmark Finance which was a 3 partner corporate conglomeration...can you guess who was one of the big 3? YEP! Goldman Sucky Sachs! Now, who owns GM? Oh Yeah! Obummer and gang!

To: princess leah

When the story of this era gets written it’s going to rival the financial and political corruption of any other period of our history.

8

posted on

04/19/2010 8:07:15 PM PDT

by

Pelham

(Obamacare, the new Final Solution.)

To: Pelham

Wall Street investment banks weren’t subject to regulations forcing them to make loans. No, but they speculated on the garbage the Gov't was perpetrating on the mortgage banks. Speculators have a way of speculating on what's out there, y'know?

If someone did something illegal, go get them. But the biggest shysters were Dodd, Frank and Cuomo IMO who out of one side of their mouth forced atrocious loans, then out of the other said the nation's finances were fabulous while forcing the taxpayer to bear the burden of the laws they pushed.

To change the rules forever now by creating draconian Gov't oversight boards because of laws the Gov't PASSED IN THE FIRST PLACE is typical of the anti-capitalist clowns who are running things. I suspect that the 2 Repub SEC officials who voted against the GS action are thinking along the same lines.

9

posted on

04/19/2010 8:07:56 PM PDT

by

what's up

To: NormsRevenge

10

posted on

04/19/2010 8:21:03 PM PDT

by

tarpit

To: Pelham

My take is that Goldman and 0bama both like this action. This is a civil case slap on the wrist for Goldman that will take years to pan out. Make 0bama look tough on the banksters. Meanwhile the banksters are piling up a higher tower of credit default swaps and have their high frequency trading scam in high gear

GS gets to look like “these bastards are finally getting punished”. The truth is far from that.

11

posted on

04/19/2010 8:21:21 PM PDT

by

dennisw

(It all comes 'round again --Fairport)

To: Pelham

Crime pays, especially if you have the juice to insure that laws get changed to protect you.

Dear Mr. Lee: I was previously employed by Argent Mortgage for two and a half years and managed, among other areas, the corporation's fraud investigation, borrower complaints and repurchase departments. There are currently over 568 open fraud investigations involving hundreds of brokers and hundreds of millions of dollars in fraudulent loans that are being covered up by top executives in the company. If a broker sustains a certain monthly volume, Argent management looks the other way and, not only does not suspend the bad brokers, but knowingly sells these fraudulent loans on the secondary market to unwitting investors.

I was terminated today and left with just my purse in tow, but I have names of individuals in the company who need to be served with subpoenas to enable them to turn over their spreadsheets and boxes full of documentation and evidence of all the fraud they have found that is being covered up by Argent Mortgage's executive management. The state regulators need to know the truth about the blind eye Argent turns to the fraud perpetrated on innocent consumers by high volume brokers. They also need to be aware that Argent knowingly bundles these fraudulent loans and sells them as mortgage-backed securities on Wall Street, thereby compromising the SEC, as well as our country's economic stability.

At a recent fraud seminar attended by hundreds of mortgage lenders in Washington D.C. a week ago, an attorney who works for Argent's retained law firm, Buchalter Nemer, stood up and told the seminar attendees that the wholesale lenders in the audience had better beware, unless their name is Argent. Argent is safe from investigation because the government got their $325 million settlement from Ameriquest and won't be looking into Argent, per the settlement agreement. I hope this isn't true because Argent Mortgage funded over $50 billion in 2005 and is gearing up to fund well over $80 billion dollars of fraudulent loans in 2007.

and....

Nothing to see

there... move along....

12

posted on

04/19/2010 8:22:26 PM PDT

by

LomanBill

(Animals! The DemocRats blew up the windmill with an Acorn!)

To: what's up

“No, but they speculated on the garbage the Gov’t was perpetrating on the mortgage banks.”

I assume you mean mortgage banks like Ameriquest, Countrywide, and Argent, which dominated the subprime market. They in effect invented it. But like the Wall Street investment banks they weren’t subject to CRA regulation. Only depository institutions were.

“IMO who out of one side of their mouth forced atrocious loans, “

Your opinion here is based in error. CRA doesn’t mean subprime. And even when CRA loans were subprime they were conforming loans, a type which isn’t risky and isn’t high yield. The high risk paper was a type invented by Wall Street and the subprime mortgage houses for the express purpose of generating high yield paper. These were Option ARMs, Stated Income Stated Asset, 125% of value, every sort of high risk loan imaginable.

“To change the rules forever now by creating draconian Gov’t oversight boards because of laws the Gov’t PASSED IN THE FIRST PLACE is typical of the anti-capitalist clowns who are running things”

You are building a straw man argument. The problem isn’t “laws the gov’t passed in the first place”; the problem is “laws the gov’t got rid of in 1999 during the Clinton administration”. The Glass Steagall act was passed in the 1930s to keep investment banks out of the world of commercial banking. It’s not a coincidence that less than a decade after repealing Glass Steagall that Wall Street is again involved in something resembling the Depression. We need a return to Glass Steagall or something like it.

13

posted on

04/19/2010 8:27:30 PM PDT

by

Pelham

(Obamacare, the new Final Solution.)

To: dennisw

I agree. It’s kabuki designed to fool us rubes.

I’m just hoping that the rise of the Tea Party means that we rubes aren’t so easy to fool.

14

posted on

04/19/2010 8:29:57 PM PDT

by

Pelham

(Obamacare, the new Final Solution.)

To: what's up; Pelham

[No, but they speculated on the garbage the Gov't was perpetrating on the mortgage banks. ]

The Government didn't "perptrate" anything on Argent Mortagage/Ameriquest - in fact, it was more the other way around as...

R.I.N.O.

R.I.N.O.

A Republic is a system, of governance characterized by the Rule of Law.

When the Law fails, the Republic fails.

Why just eat a few golden Acorns when you can cook the whole goose? Ooops.

15

posted on

04/19/2010 8:32:35 PM PDT

by

LomanBill

(Animals! The DemocRats blew up the windmill with an Acorn!)

To: LomanBill

Good find. Most people have no idea how corrupt the mortgage markets had become during the bubble. The people at the top did, and they fired any Old Style employees who had the integrity to object to what was going on.

16

posted on

04/19/2010 8:33:27 PM PDT

by

Pelham

(Obamacare, the new Final Solution.)

To: LomanBill

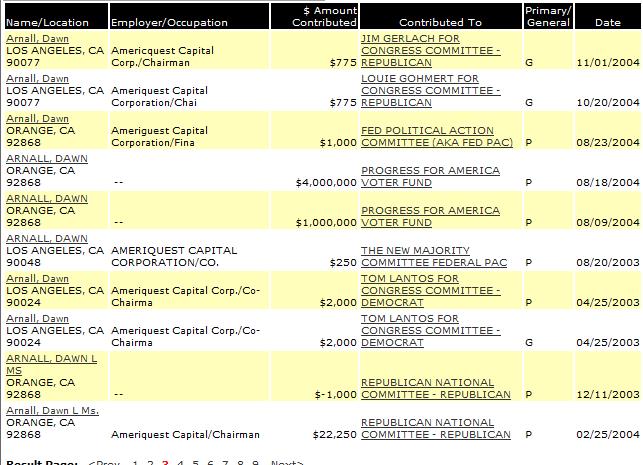

Another good find. Arnall knew who to pay off to make sure that no one interfered with the game.

17

posted on

04/19/2010 8:37:06 PM PDT

by

Pelham

(Obamacare, the new Final Solution.)

To: Pelham

Good find. Most people have no idea how corrupt the mortgage markets had become during the bubble. The people at the top did, and they fired any Old Style employees who had the integrity to object to what was going on.During the height of the mania you had Lehman, Merrill and others screaming down to their mortgage brokers. Demanding more mortgages of any/every kind to fill up ready made tranches. They even gave the mortgage brokers more favorable terms to accelerate the process. Part of the reason you had all those low-doc, no-doc, adjustable rate mortgages

18

posted on

04/19/2010 8:40:41 PM PDT

by

dennisw

(It all comes 'round again --Fairport)

To: Pelham

>>The people at the top did

"But but ve vaz just following Der Vizard's rules"

"We didn't truly know the dangers of the [Derivatives] market, because it was a dark market," says Brooksley Born, the head of an obscure federal regulatory agency -- the Commodity Futures Trading Commission [CFTC] -- who not only warned of the potential for economic meltdown in the late 1990s, but also tried to convince the country's key economic powerbrokers to take actions that could have helped avert the crisis. "They were totally opposed to it," Born says. "That puzzled me. What was it that was in this market that had to be hidden?"

19

posted on

04/19/2010 8:45:02 PM PDT

by

LomanBill

(Animals! The DemocRats blew up the windmill with an Acorn!)

To: NormsRevenge

It will take some time and resources to dig into this real deep, but you have to ask yourself what, if any, was the relationship between paulson and ingato.

Tuesday, February 12, 2008

ACA sells CDO business to avert disaster

(FT Alphaville) Monoline ACA isn’t the largest in the world, but its failure would have been extremely painful for banks.

Since it only started out with an A rating, ACA had collateral posting requirements written into its numerous CDS positions. Thus in the event of a downgrade, not only did ACA risk losing new business, but insolvency too, since posting sufficient collateral was impossible.

A big downgrade and two waivers on posting that collateral later and the worst case scenario for ACA might just have been averted.

The monoline is being broken up - selling off its CDO and CLO management businesses. That in turn may raise enough cash for the monoline to meet capital requirements for its actual bond insurance business. And by that, saving Merrill Lynch, for one, $6.6bn.

But will it be enough? ACA, by some counts, has an awful lot of collateral to raise. Before Christmas, the bond insurer needed $1.7bn to post against CDS on CDOs. That was based against super-senior CDO tranches valued at 93 per cent of face. As AIG this week discovered, it’s important to value those super-senior positions correctly. By some estimates, they’re now worth 60 per cent of face. Which would push ACA’s required collateral pledges to $10bn.

Here, anyway, is the ACA statement:

ACA Financial Guaranty Corporation, a subsidiary of ACA Capital Holdings, Inc. (OTC BB: ACAH.PK), announced today that it has entered into a letter of intent with FSI Capital, LLC (”FSI Capital”) to sell its U.S. ABS and Corporate Credit CDO asset management business. FSI Capital, through its affiliates and subsidiaries, manages 17 CDOs totaling approximately $7.5 billion.

The Company also announced today that it has entered into a letter of intent with Resource Financial Fund Management, Inc. (”RFFM”), a wholly-owned subsidiary of Resource America, Inc., and the parent company of Apidos Capital Management, LLC, to sell its U.S. CLO asset management business. Apidos Capital Management has closed 8 CLOs with approximately $2.8 billion of assets under management.

Each of the transactions is subject to final due diligence, the negotiation and execution of a definitive agreement and other standard conditions.

About FSI Capital

FSI Capital is a leading alternative fixed income asset management company focused on financial services, structured finance and real estate. Together with its affiliated companies, FSI Capital has over 40 employees in four offices in the United States. FSI Capital is affiliated with a registered investment adviser.

About Resource America, Inc.

Resource America, Inc. is a specialized asset management company that uses industry specific expertise to generate and administer investment opportunities for its own account and for outside investors in the commercial finance, real estate and financial fund management sectors. As of November 30, 2007, the company had assets under management of $17.3 billion. RFFM is a registered investment adviser.

20

posted on

04/19/2010 8:47:31 PM PDT

by

tarpit

Navigation: use the links below to view more comments.

first 1-20, 21-25 next last

Disclaimer:

Opinions posted on Free Republic are those of the individual

posters and do not necessarily represent the opinion of Free Republic or its

management. All materials posted herein are protected by copyright law and the

exemption for fair use of copyrighted works.

FreeRepublic.com is powered by software copyright 2000-2008 John Robinson