Skip to comments.

Uh, Oh: Mortgage Refis Plunge

Townhall.com ^

| June 12, 2013

| Mike Shedlock

Posted on 06/12/2013 5:10:53 AM PDT by Kaslin

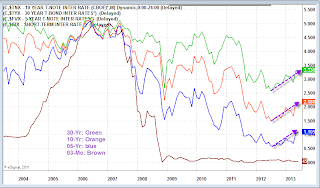

Curve Watchers Anonymous has been watching the rise in interest rates across much of the yield curve.

Yield Curve as of 2013-06-11

click on chart for sharper image

As one should suspect, mortgage rates have been rising in conjunction with the rise in treasury rates. Here is a chart from Steen Jakobsen, Chief economist at Saxo Bank in Denmark.

Note the annotation "30 Yr mortgages rate is up 76 basis points on the year with no growth increase". the phrase "no growth" pertains to lack of growth in the overall US economy.

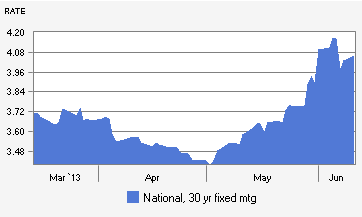

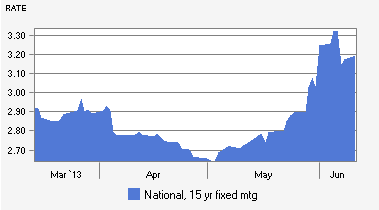

BankRate notes the following 3-month trends.

30-Year Mortgage Rate

15-Year Mortgage Rate

5/1 ARM Mortgage Rate

As one might suspect this rapid rise in mortgage rates will wreak havoc on mortgage refinancing. And it did. I called a couple of my industry contacts and they state refinancings have plunged by 50% or more.

One contact says there has been spillover into new home applications, another has not seen that "yet".

Word About Convexity

As rates rise, three things happen.

- Refinancings plunge

- Losses mount

- Hedging increases

Bloomberg discusses convexity hedging in its report

TOPICS: Business/Economy; Culture/Society; Editorial

KEYWORDS:

Navigation: use the links below to view more comments.

first 1-20, 21-32 next last

More in the link

1

posted on

06/12/2013 5:10:53 AM PDT

by

Kaslin

To: Kaslin

I think I know why refi’s are “plunging” - the process isn’t going nearly as smooth as it used to.

We do some RE investing - rentals, etc.

Refi’s in the past have been a breeze.

Recently, though, I’ve been in a refi process for my own house for over 5 months.

Telling.

2

posted on

06/12/2013 5:13:50 AM PDT

by

MrB

(The difference between a Humanist and a Satanist - the latter admits whom he's working for)

To: Kaslin

Everyone and his brother has refied, at 4% or below. Unless interest on a 30 yr goes to 2% the refi market will be dead for a long time.

3

posted on

06/12/2013 5:15:42 AM PDT

by

central_va

(I won't be reconstructed and I do not give a damn.)

To: Kaslin

Here’s a “curve”.

30 yr fixed rose 0.75% in the 2 weeks we waited for the seller’s lawyer to get off of his dead butt to write the contract.

Don’t bother listing the options we might have had.....seller insisted on using her lawyer.

4

posted on

06/12/2013 5:17:40 AM PDT

by

G Larry

(Let his days be few; and let another take his office. Psalms 109:8)

To: MrB

About 3 or 4 months ago I did a VA ‘streamline’ refi on my house. Sailed through in a month. Glad I did it when I did.

5

posted on

06/12/2013 5:21:33 AM PDT

by

tgusa

(gun control: deep breath, sight alignment, squeeze the trigger .......)

To: Kaslin

A turd will only float for so long.

LLS

6

posted on

06/12/2013 5:24:14 AM PDT

by

LibLieSlayer

(FROM MY COLD, DEAD HANDS!)

To: G Larry

On paper the .75 does not sound like much BUT when one looks at the increase over where it was a month ago, it is staggering.

This is similar to rising rates around 1980. I was buying a home then, awaiting mortgage clearance, and the rates were literally going up half a point a week some weeks. Over the 3 months it took to get my mortgage “approved” rates had climbed from 9% to something like 13% and I barely qualified for that.

When the FED turns off the spigot, if not already done so, rates are going to skyrocket, the deficit will blow out of bounds due to the shortness of maturities in our indebtedness and his maximum eminence will be crying all the way to the podium to blame bankers, the FED, the GOP, and perhaps even FOX News for his bankrupt budget.

7

posted on

06/12/2013 5:31:05 AM PDT

by

Mouton

(108th MI Group.....68-71)

To: Kaslin

Folks have gotten used to low, low mortgage rates. Even a minor blip up puts people in a holding pattern until the rate comes back down. Can’t blame them. The FED has taught us that low rates are a “right”.

Unfortunately, this “blip” could very well morph into a blob. Bad news for the frail recovery of the sales market.

8

posted on

06/12/2013 5:44:23 AM PDT

by

moovova

To: Kaslin

Not to mention that PMI will be required for the entirety of the loan on FHA loans, so there is no point in doing a refi anymore if you have an FHA loan. Last year they required doubling up on PMI, now they make it a permanent fixture.

9

posted on

06/12/2013 5:55:59 AM PDT

by

jurroppi1

To: Kaslin

The topic is refinancing.

It would seem the reason for the drop off is saturation. Those who want to refinance have done so.

10

posted on

06/12/2013 6:08:39 AM PDT

by

bert

((K.E. N.P. N.C. +12 ..... Who will shoot Liberty Valence?)

To: MrB

I just finished refinancing our jumbo. In hindsight I’d rather poke sticks in my eyes than do it again.

11

posted on

06/12/2013 6:09:12 AM PDT

by

skeeter

To: skeeter

Similar situation here - refi from an ARM at 3.75 to a fixed 30 at 3.86.

12

posted on

06/12/2013 6:13:56 AM PDT

by

MrB

(The difference between a Humanist and a Satanist - the latter admits whom he's working for)

To: Kaslin

As rates rise, three things happen.

1.Refinancings plunge

2.Losses mount

3.Hedging increases

There is actually a fourth thing. It is explained in the phrase, “People don’t buy a price. They buy a monthly payment.”

I.e. an interest rate rise creates downward pressure on prices of all financed goods and services.

13

posted on

06/12/2013 6:14:42 AM PDT

by

cuban leaf

(Were doomed! Details at eleven.)

To: G Larry

Did you tell her, “never mind”?

14

posted on

06/12/2013 6:15:34 AM PDT

by

cuban leaf

(Were doomed! Details at eleven.)

To: moovova

Unfortunately, this “blip” could very well morph into a blob. Bad news for the frail recovery of the sales market.

I didn’t believe rates could possibly go up because it would be fatal to an economy already barely surviving on life support.

Apparently national suicide is the next tactic to be used by our non-elected leaders. This’ll be VERY interesting to watch, though not a lot of fun.

15

posted on

06/12/2013 6:18:04 AM PDT

by

cuban leaf

(Were doomed! Details at eleven.)

To: Kaslin

Fortunately my refi was in the pipeline, rate locked in, before rates began bouncing back.

Rates have been very low, yes, but your credit score had better be close to perfect; and your appraisal (dictating the maximum amount you can borrow) may come in shockingly low.

Fortunately, I wanted to pay down about half of my mortgage, and I wanted to go from an ARM to a fixed 10-year mortgage. My rate: 2 5/8.

:-)

16

posted on

06/12/2013 6:30:14 AM PDT

by

southernnorthcarolina

("Better be wise by the misfortunes of others than by your own." -- Aesop)

To: cuban leaf

Gubment had to keep rates down for awhile. There were a lot of rate resets still in the pipeline. Had to give those mortgage holders time to refinance at the lower rates. Otherwise, automatically resetting to higher rates would've brought another mega-round of foreclosures...

17

posted on

06/12/2013 6:38:34 AM PDT

by

moovova

To: MrB

Heck, we have 820s credit ratings borrowing than less than I make in a year for a house with very little DEBT and it took 5 months to close. Just simply stupid crap happening in the market right now....

18

posted on

06/12/2013 6:49:24 AM PDT

by

fuente

(Liberty resides in three boxes: the ballot box, the jury box and the cartridge box--Fredrick Douglas)

To: MrB

Heck, we have 820s credit ratings borrowing than less than I make in a year for a house with very little DEBT and it took 5 months to close. Just simply stupid crap happening in the market right now....

19

posted on

06/12/2013 6:50:07 AM PDT

by

fuente

(Liberty resides in three boxes: the ballot box, the jury box and the cartridge box--Fredrick Douglas)

To: fuente

Dittos... I’m not in too much of a hurry, though.

The monthly is currently lower on the ARM than it will be on the fixed, and it doesn’t adjust for quite a while.

I’m just gambling that the fixed rates are going up soon.

20

posted on

06/12/2013 6:52:33 AM PDT

by

MrB

(The difference between a Humanist and a Satanist - the latter admits whom he's working for)

Navigation: use the links below to view more comments.

first 1-20, 21-32 next last

Disclaimer:

Opinions posted on Free Republic are those of the individual

posters and do not necessarily represent the opinion of Free Republic or its

management. All materials posted herein are protected by copyright law and the

exemption for fair use of copyrighted works.

FreeRepublic.com is powered by software copyright 2000-2008 John Robinson