Skip to comments.

What Core Labs Tells Us About The 'Second Wave' Shale Plays

seekingalpha ^

| May. 19, 2014 2:26 PM ET

| Casey Hoerth

Posted on 06/18/2014 9:30:03 AM PDT by ckilmer

Sampling and analysis activity picking up in newer shale plays.

After a steep drop in stock price, Core's valuation is reasonable once again.

Core Laboratories (NYSE: CLB), a mid-cap oil servicer focusing on production enhancement and research optimization, has recently been savaged since giving lower revenue and earnings guidance. Core lowered full-year earnings guidance from $6.00-$6.25 to $5.80-$6.00 per share. Revenue for the second quarter is now estimated to be between $265 and $270 million; a number less than the previous estimate, but still above last year's second quarter results. The analysts estimated revenue to be around $288 million.

(Excerpt) Read more at seekingalpha.com ...

TOPICS: Business/Economy

KEYWORDS: corelabs; energy; fracking; oil

1

posted on

06/18/2014 9:30:03 AM PDT

by

ckilmer

To: thackney; bestintxas; Kennard; nuke rocketeer; crusty old prospector

Decline led by original shale plays

Management's primary reason for its downward revision was disappointing volume in core sampling and analysis in some of the older shale plays. North American clients in more developed shale plays, such as the Bakken, Niobrara and Eagle Ford, are now sampling and analyzing less reserve fluids than previously expected.

As these three shales mature, demand to understand the geology and flow rate also decreases. It makes sense, then, that Core is also beginning to get inquiries about enhanced recovery techniques from shale clients. Going forward, operators in the Eagle Ford, Bakken and Niobrara will spend much less on exploration, appraisal and land-buying, and more on maximizing ultimate recovery. While Core is quite a diversified company, and will surely benefit in this scenario as well as the last, the company has seen a temporary negative effect from this switch.

The second wave

On a positive note, management saw increased core sampling and analysis in some of the newer plays, namely the SCOOP (south central Oklahoma), the Tuscaloosa Marine Shale, and most of all the Wolfcamp. These three, I believe, will be the leading 'second wave' shale plays in North America.

However, the increase in activity here was also not enough to offset the decline in activity in the older shale plays. In other words, the acreage rush that took place in the Bakken and Eagle Ford has yet to materialize to an equal degree in the Wolfcamp and Tuscaloosa Marine.

That is because the situation today is far different from that in 2010. After the Bakken and Eagle Ford ramp-ups, operators are hesitant to add yet more capacity from two or three new shale plays, fearing that doing so would tip the supply and demand balance, and perhaps even lead to an 'oil glut.' Having learned its lesson in the 1980s, the oil and gas industry is adamant to avoid making that mistake again. Hence, I believe, the caution we see today.

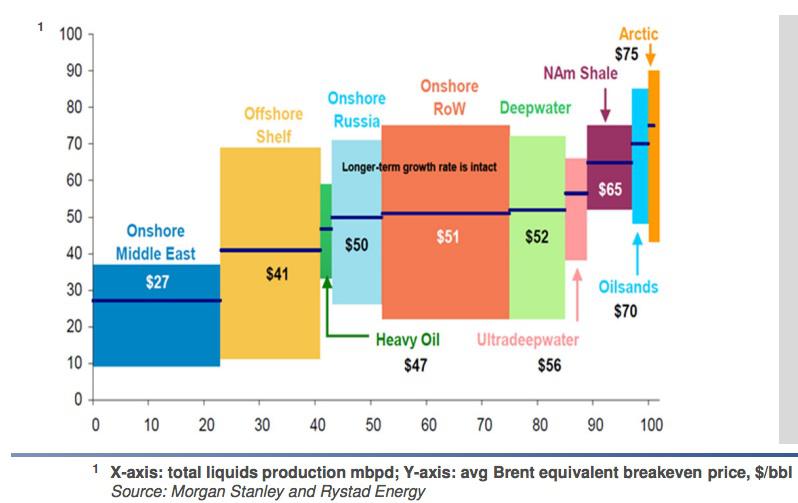

(click to enlarge)

Courtesy of Seadrill Investor Relations

This chart above is of 'breakeven' prices from various forms of liquids production. I believe this gives us a 'big picture' view. North American shale is, as you can see, still a relatively small part of the overall supply picture. Frankly, I think that this chart ought to be broken down into a few more pieces. For example, "Onshore rest of world" includes in it marginal producing regions such as Nigeria, Venezuela and Khazakstan. Breakevens in these places should be far higher than the $51 per barrel average shown here. And that $51 is likely brought down by very low-cost water floods and CO2 floods in North America, in which costs of production rival the Onshore Middle East average.

The point is this: While North American Shale may look like one of the more marginal, high-cost producers according to this chart, it really isn't. In addition, this $65 average breakeven includes lower-quality shale plays such as the Granite Wash, Mississippi Lime and Utica, neither of which have worked out very well. If we were take just the Eagle Ford, Bakken and Niobrara, that $65 breakeven would be much lower.

I believe the same logic can apply to the 'second wave' shale plays, especially the Wolfcamp and Tuscaloosa Marine Shales. Just a cursory look into both of these shales reveals that the better acreage positions are basically going to develop no matter what.

Concho Resources (CXO), one of the companies holding acreage in the core 'Wolfcamp A' area, has a breakeven of just $41.25. Relating that to the chart above, Concho's Wolfcamp operations are more profitable than onshore Russia, and about as profitable as offshore, shallow-water operations.

Looking over at the Tuscaloosa Marine Shale, the biggest core acreage holder is Goodrich Petroleum (GDP), a $1 billion company. Currently, Goodrich's breakeven is between $51 and $68 per barrel, depending upon the well type. While this is not yet as promising as the Wolfcamp, management expects that, within a couple years at the most, its engineers can reduce well completion costs to move breakevens to between $41 and $54 per barrel. That's more like it. Once again, the core acreage of the Tuscaloosa Marine Shale will be more profitable than the oil sands, deepwater oil, ultra deepwater oil and some of onshore Russia.

2

posted on

06/18/2014 9:35:34 AM PDT

by

ckilmer

(q)

To: thackney; bestintxas; Kennard; nuke rocketeer; crusty old prospector

On a positive note, management saw increased core sampling and analysis in some of the newer plays, namely the SCOOP (south central Oklahoma), the Tuscaloosa Marine Shale, and most of all the Wolfcamp. These three, I believe, will be the leading ‘second wave’ shale plays in North America.

3

posted on

06/18/2014 9:37:37 AM PDT

by

ckilmer

(q)

To: ckilmer

Do you see anything in this article that remotely matches the title?

4

posted on

06/18/2014 9:41:50 AM PDT

by

thackney

(life is fragile, handle with prayer)

To: thackney

Do you see anything in this article that remotely matches the title?

......................

The second wave

On a positive note, management saw increased core sampling and analysis in some of the newer plays, namely the SCOOP (south central Oklahoma), the Tuscaloosa Marine Shale, and most of all the Wolfcamp. These three, I believe, will be the leading ‘second wave’ shale plays in North America.

5

posted on

06/18/2014 10:08:52 AM PDT

by

ckilmer

(q)

To: ckilmer

I don’t see that telling anything about the “second wave” beyond a possible, only possible, existance of a second wave.

6

posted on

06/18/2014 10:10:47 AM PDT

by

thackney

(life is fragile, handle with prayer)

To: thackney

I don’t see that telling anything about the “second wave” beyond a possible, only possible, existance of a second wave..............

Core labs doesn’t do discovery. Core Labs does optimization.

Core Labs does the optimization for wells. They’re the ones that enable the companies to optimize them. They call themselves the “reservoir optimization company.”

http://www.corelab.com/#

Three years ago Core Labs work was mostly in Bakken, Niobrara and Eagle Ford. Now demands for their services are down in those fields as they move from exploration to production.

That Core Labs is getting rising inquiries about SCOOP (south central Oklahoma), the Tuscaloosa Marine Shale, and most of all the Wolfcamp....

That means the oil companies are most interested in optimizing these formations.

Could it be that other formations are just as promising but don’t need Core Labs services? Yes.

However, because the call for Core Labs services is declining in the Baaken Eagle Ford and Niobrara—and increasing in Scoop Oklahoma, Tuscaloosa Marine Shale and Wolfcamp—its reasonable to think that the latter three plays will enjoy large gains in production sometime in the future.

7

posted on

06/18/2014 10:42:01 AM PDT

by

ckilmer

(q)

To: ckilmer

I understand Core Labs and what they do and why it is needed.

because the call for Core Labs services is declining in the Baaken Eagle Ford and Niobrara—and increasing in Scoop Oklahoma, Tuscaloosa Marine Shale and Wolfcamp—its reasonable to think that the latter three plays will enjoy large gains in production sometime in the future.

Until the increases in the new field exceed the decreases in the older fields, there is no second wave.

8

posted on

06/18/2014 10:58:08 AM PDT

by

thackney

(life is fragile, handle with prayer)

To: ckilmer

Operations are gearing up south of the boarder in the Eagle Ford. When that Mexican oil comes on line who knows were the price per barrel will go.

9

posted on

06/18/2014 11:01:24 AM PDT

by

2001convSVT

(Going Galt as fast as I can.)

To: 2001convSVT

Operations are gearing up south of the boarder in the Eagle Ford.

- - -

Not much going on yet.

- - - - -

Pemex seeking partners for Eagle Ford and deep-water work

http://fuelfix.com/blog/2014/05/06/pemex-seeking-partners-for-eagle-ford-and-deep-water-work/

Hernandez-Garcia said Pemex has only recently started drilling a few unconventional wells but needs the participation of partners to be competitive. He added that Pemex doesn’t have the level of technical expertise to succeed on its own in those areas.

- - - - - - - -

Mexico’s Subsurface Presents New E&P Opportunities

http://theeaglefordshale.com/tag/pemex/

An assessed 60 billion boe of shale oil and gas resources lie in four areas: the extension of the S. Texas Eagle Ford trend into northern Mexico and the Upper Jurassic organic-rich shales in the Sabinas basin, the western margin of the Burgos basin, and in the Tampico basin. Pemex has been carefully testing the potential of these areas with pilot wells but so far have been unable to demonstrate viable economics.

As the company lacks the required expertise, these plays will probably be licensed out. The problem for newcomers will be to locate the sweet spots for hydrocarbon liquids, avoiding the gassy and less prolific areas, in order to apply their technological experience profitably.

10

posted on

06/18/2014 11:29:09 AM PDT

by

thackney

(life is fragile, handle with prayer)

To: 2001convSVT

that’s three or four maybe five years away.

11

posted on

06/18/2014 3:06:37 PM PDT

by

ckilmer

(q)

To: thackney

Until the increases in the new field exceed the decreases in the older fields, there is no second wave.

............

the eagle ford & bakken are not going to decrease but after the end of 2015 or there about— according to the EIA—their rate of increase of production will slow down considerably. What we have seen is that their rate of increase will slow down to about an extra 100,000 Barrels@day annually from 2016-2020.

Some of the other fields especially the oklahoma fields may get to the point by 2016 where their rate of production increase exceeds that of the baaken and eagle ford which by then would be slowed down to an an extra 100,000 Barrels@day annually. So the oklahoma fields would be producing more than 100,000 k annually for a couple years. But the article mentions wolfcamp in the permian basin as the place where optimization is most especially taking place. That’s the place where some big annual increases may be realized. But we just don’t know yet. That’s the biggest story of the next year or so. Will the Permian basin live up the hype/promise.

12

posted on

06/18/2014 3:18:06 PM PDT

by

ckilmer

(q)

To: thackney

namely the SCOOP (south central Oklahoma), the Tuscaloosa Marine Shale, and most of all the Wolfcamp. These three, I believe, will be the leading ‘second wave’ shale plays in North America.

.............

the one part of that that didn’t quite make sense is the Tuscaloosa Marine Shale. Whereas Both the Oklahoma and the Permian basis are already showing rising to sharply rising oil production—for which Core Labs optimization would make sense.... the Tuscaloosa Marine Shale oil production in Louisiana is flat.

http://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=MCRFPLA1&f=M

Mississippi is not much better.

http://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=pet&s=mcrfpms1&f=m

I’ve read recently promising stories about drillers getting some successes out the Tuscaloosa Marine Shale but EIA numbers show that whatever is happening in this formation is all preliminary.

Maybe Core Labs has a big imaging division apart from their optimization division. So the interest they’re seeing out of the Tuscaloosa Marine Shale drillers is all about trying to get their arms around what’s below ground rather than optimizing their drilling processes.

13

posted on

06/19/2014 9:23:52 AM PDT

by

ckilmer

(q)

To: thackney

Here’s the answer as to why Core Labs is getting rising business out of the TMS formation

............................’’

‘’Meanwhile, Goodrich Petroleum’s CEO provided a bit more color on his outlook for the TSM during the Q-and-A portion of the firm’s Aug. 4 conference call:

We’re very comfortable today with what we see from a geologic standpoint of going ahead and drilling wells. In fact we don’t really even see much need, at least in most of our acreage, for pilot holes. There [are] sufficient amounts of historical vertical wells that have been drilled through the Tuscaloosa Marine Shale that we’re comfortable going out and drilling today. I would characterize at least in our view that the sole or the largest single risk to the play is just one of the economic performance versus well costs. We know the Tuscaloosa is present, sufficiently thick, thoroughly oil saturated. It’s just a little unproven in that no one has drilled yet a well that’s demonstrated in the EUR horizontally that would match up to costs. And that’s just [be]cause there haven’t been really many or any of them out there that have done that.

http://www.gohaynesvilleshale.com/group/tuscaloosamarineshale/forum/topics/tms-headlines

14

posted on

06/19/2014 11:30:43 AM PDT

by

ckilmer

(q)

Disclaimer:

Opinions posted on Free Republic are those of the individual

posters and do not necessarily represent the opinion of Free Republic or its

management. All materials posted herein are protected by copyright law and the

exemption for fair use of copyrighted works.

FreeRepublic.com is powered by software copyright 2000-2008 John Robinson