Skip to comments.

4th of July: Salute to Shale New Study Shows That W/o Fireworks, a 1980s Deja Vu Could Be Inevitable

Fuel Fix ^

| July 1, 2013

| Amy Myers Jaffe

Posted on 07/01/2013 7:29:44 AM PDT by thackney

Full Title: Happy 4th of July: A Salute to Shale…New Study Shows That Without Fireworks, a 1980s Deja Vu Could Be Inevitable

Signs are on the horizon that oil prices could take a tumble, should war drums stop beating in the Middle East. High oil prices, no matter how permanent they might seem, eventually stimulate downward structural changes in oil demand. And, just like the 1980s, rising capital investment in oil exploration and technological progress is ushering in new oil supplies.

So far, a repeat of the 1980s has been avoided given loose US monetary policy and the glamour of China’s magnificent economic rise. But it would be a mistake to assume that the oil price euphoria of 2007-2008 will not, at some point, be followed by a long-term adjustment similar to the 1980s oil price collapse. This is the key finding to wavelet analysis by my co-author Mahmoud El Gamal. Our new working paper “Oil Demand, Supply and Medium-Term Price Prospects: A Wavelet-based Analysis”(click publications) forecasts a significant fall in oil prices in the 3 to 5 year time horizon, barring a major war in the Middle East that destroys infrastructure.

The market responses of consumers and governments to high oil prices are always hard for industry and OPEC countries to internalize. The inelastic nature of short term oil demand tends to mask structural changes. But the handwriting is on the wall. Governments around the world have been responding for years now to rising energy costs with substantial policy changes, and a downward spiraling tipping point is inevitable –usually just when oil producers get confident that the new higher price ranges are here to stay.

As our paper shows, the reality is a 31 % decline in the energy intensity of real economic output has taken place in the last two decades, and we can expect this rate of decline to accelerate further, the longer prices stay high. Mandated improvements in automobile efficiency are just the tip of the iceberg. So far, oil prices have failed to fall below their mean level for any extended time in recent years due in part to the unprecedented and coordinated expansionary monetary policies of central banks from around the world. But as we argue in the paper, these unconventional monetary policies have held commodity prices, especially oil, too high for a strong recovery to take place. Eventually, gravity will set in. A brief hint of what such downward pressures might look like came about in earlier this month when markets became fearful of a liquidity crunch might be forthcoming in China.

High oil prices have also given energy companies and institutional investors the funds and the incentive to explore more expensive oil production technologies and alternative energy. In a perfectly competitive market, it would be reasonable to assume that oil prices were rising to signal the depletion of lower cost reserves and the profitability of moving to higher cost resources. However, the global oil industry does not fully conform to this theoretical model of a competitive natural resource market. Instead, lack of access to lower cost resources, partly driven by OPEC policies and partly by non-competitive or inefficient practices of national oil companies, has forced private capital to seek other options. As prices rose, investors were signaled that new technologies could be applied at reduced risk and the euphoria of the perceived oil scarcity panic (ala Peak Oil Theory) ensured that capital markets were ready to pony up near unlimited funds to the bonanza of a resource technology experiment.

In the case of the post 1970s oil shocks, a concentration of capital from financial players extending from the Edinburgh investment trusts to private investors like Lord Thomson, a British newspaper tycoon, rushed to the North Sea market a new generation of technology that was heretofore in the development phased, allowing companies to work through water depths that had never been tried before. The industry created drilling technologies and platforms that could withstand waves ninety feet high and winds as gusty as 130 miles per hour. New platforms that were as large as small industrial cities, set on man-made islands, were developed and over time, production costs fell from $25 a barrel to as low as $3 to $5 a barrel. Average North Sea oil output climbed from 2.7 million b/d at the start of 1983 to nearly 3.9 million b/d by early 1988, putting OPEC under tremendous pressure. Across the pond in the United States, Wall Street also stepped up to the plate in the 1990s with a ready arsenal of derivative products to allow the exploitation of hard to reach assets in deep oceans and on the Arctic shelf. Firms like Baker’s Trust offered synthetic hedges to Shell Oil and others to lock in profits from technically risky prospects.

In the oil price euphoria of the 2000s, the master limited partnership (MLP) format ushered in a gigantic flow of institutional money to resource development from the shale formations of the United States. The result has been that dire predictions that world oil production rates would begin to fall steeply in the 2000s did not, in fact, materialize.

Instead, as in the late 1970s and early 1980s, high prices increased the incentives for technological innovation in the oil patch. This time around the results may prove to be nothing less than stunning. At some point, even Peak oil stalwarts will have to abandon the conventional wisdom that as mature fields would become rapidly depleted in the Western world, the last remaining barrels will be found in the prolific basins of Middle East, leaving the West in the clutches of OPEC. Shale means that this mantra will be proven wrong once again. Tight oil, that is unconventional oil from shale structures, is developing at an extraordinarily rapid rate in the United States, and U.S. analysts are now projecting that US oil production could rise significantly over the next decade. Estimates range from an increase on of 3 million to 10 million b/d of oil and natural gas liquids production from shale formations by 2020, with some analysts projecting that the United States could become an exporter of natural gas liquids and even crude oil over time.

Up until recently, the possibility that artificial and geopolitical barriers to resource exploitation in the Middle East and Russia had imposed short term conditions was dismissed as the optimism of academic economists. But as time goes on, it will become all the more clear that oil producers in the Middle East and Russia have once again failed to assess that by creating a temporary scarcity premium, they have risked hastening a return to a downward price cycle that has reemerged from decade to decade with the general business cycle.

Like the 1980s, OPEC will soon have to pick between maintaining its global market share or defending prices. The longer that OPEC acts to hold oil prices at today’s lofty levels, the more investors will rush to bring on more tight oil structures around the world, adding to already apparent supply competition. At the same time, high prices will continue to bring structural demand destruction, making it harder and harder to avoid a price collapse in the long run. The simmering proxy war in Syria between Saudi Arabia and Qatar (with “sympathy” from the United States) on the one hand, and Russia and Iran on the other, is preventing market fundamentals from asserting themselves. But any sign of a ceasefire is bound to take the steam out of the oil market, giving all players concerned less incentive to engage in serious conflict resolution.

TOPICS: News/Current Events

KEYWORDS: energy; oil

1

posted on

07/01/2013 7:29:44 AM PDT

by

thackney

To: thackney

What do you think of this Thack?

2

posted on

07/01/2013 7:37:15 AM PDT

by

headstamp 2

(What would Scooby do?)

To: headstamp 2

a long-term adjustment similar to the 1980s oil price collapse While a price collapse could happen, I don't see any way for it to be long term without a horrible long term crash in global economy.

3

posted on

07/01/2013 7:41:17 AM PDT

by

thackney

(life is fragile, handle with prayer)

To: thackney

Signs are on the horizon that oil prices could take a tumble, should war drums stop beating in the Middle East.This is interesting in light of the fact that we import virtually no oil from the ME. I'm aware that the low information voters all think that our oil comes from the ME, but most of it is from Venezuela and Canada, these days.

As for the oil "shortage" of the 1980s, it was concocted by the oil companies to drive prices up. My dad worked for the Federal Trade Commission at the time and was assigned to investigate the claims of the oil and gas producers. What he found was oil storage tanks full to overflowing and oil tankers were required to anchor out of sight over the horizon where John Q. Public could not see them because there was no place to offload the oil . However, another FReeper's dad was an airline pilot who flew out of LAX and he saw them parked out of sight.

4

posted on

07/01/2013 7:43:12 AM PDT

by

DustyMoment

(Congress - another name for the American politburo!!)

To: DustyMoment

5

posted on

07/01/2013 7:55:41 AM PDT

by

thackney

(life is fragile, handle with prayer)

To: thackney

B0 will do everything he can to block energy production.

If energy prices decline, watch B0 take all the credit. Mittens should have mopped the floor with Soetoro in the energy debate, but let 0 wriggle off the hook.

The narrative becomes reality. Just like Clinton claiming credit for His “great” economic boon. Before he took office the recession was over — peace dividend and dot com bubble were in place. Before he left office a new recession had begun.

6

posted on

07/01/2013 7:57:33 AM PDT

by

Zuse

To: DustyMoment

Sorry, hit post too soon.

From the same link, you can see we get more oil from Saudi Arabia than from Venezuela and have for some time.

7

posted on

07/01/2013 7:57:38 AM PDT

by

thackney

(life is fragile, handle with prayer)

To: thackney

The domestic oil supply will disappear if oil is less than $80/bbl, so supply would dry up and price go up again.

Also, dometic prices are artificially low due to the inability to export oil.

8

posted on

07/01/2013 8:49:34 AM PDT

by

TheThirdRuffian

(RINOS like Romney, McCain, Dole are sure losers. No more!)

To: TheThirdRuffian

Also, dometic prices are artificially low due to the inability to export oil. We do export a little, usually to the closest refinery in Canada. But we still import quite a bit so there is no reasonable reason to think we could be a net exporter soon.

9

posted on

07/01/2013 9:01:26 AM PDT

by

thackney

(life is fragile, handle with prayer)

To: thackney

It’s actually illegal to export; I presume there is some sort of waiver re: a border refinery.

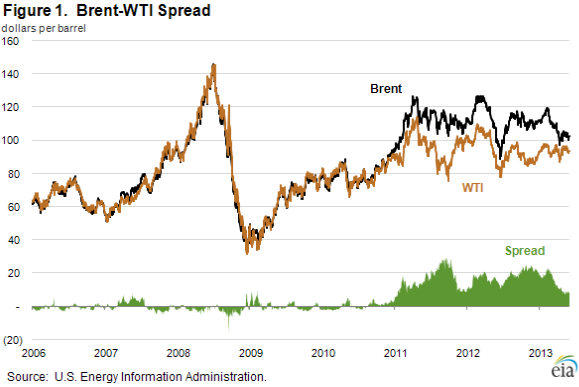

But the spread between domestic (95ish) and BRent (115ish) is absurd. You know coastal Texas people would export in a second.

Oil would have to drop $20 for the price to change domestically.

10

posted on

07/01/2013 12:43:15 PM PDT

by

TheThirdRuffian

(RINOS like Romney, McCain, Dole are sure losers. No more!)

To: TheThirdRuffian

Crude oil exports are restricted to: (1) crude oil derived from fields under the State waters of Alaska’s Cook Inlet; (2) Alaskan North Slope crude oil; (3) certain domestically produced crude oil destined for Canada; (4) shipments to U.S. territories; and (5) California crude oil to Pacific Rim countries.

http://www.eia.gov/dnav/pet/pet_move_expc_a_ep00_eex_mbbl_m.htm

Alaskan North Slope Crude Oil was banned from export until 1995 with the West Coast oil glut. About 5% was exported until 2000. None is exported since but it is still legal, just not cost effective while our west coast is importing more than Alaska produces.

11

posted on

07/01/2013 1:16:29 PM PDT

by

thackney

(life is fragile, handle with prayer)

To: TheThirdRuffian

Brent and WTI were not spread in price due to export limitations. The rules have not changed although the spread grew and is now coming back together.

Key factors behind the recent narrowing in the Brent-WTI Spread

http://www.eia.gov/oog/info/twip/twiparch/2013/130605/twipprint.html

Also the spread exists because the US is importing Brent into the US to help meet our demand. If our production rose to where we were a net exporter, the market would change.

WTI has been at a discount because it is landlocked with insufficient pipeline capacity. It is not a factor of export rules.

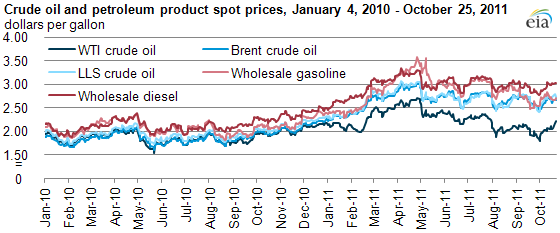

Look at the similar quality Louisiana Light Sweet delivered to St. James Louisiana. It is on the coast and has kept price match with Brent.

The article linked below is a bit dated, but it shows how LLS stayed with Brent while WTI fell below.

Recent gasoline and diesel prices track Brent and LLS, not WTI

http://www.eia.gov/todayinenergy/detail.cfm?id=3670

12

posted on

07/01/2013 1:24:35 PM PDT

by

thackney

(life is fragile, handle with prayer)

To: TheThirdRuffian

This will explain the WTI / Brent better than I did.

Brent-WTI Spread Shrinks to $5 for First Time in 2 1/2 Years

http://www.bloomberg.com/news/2013-07-01/brent-wti-oil-spread-shrinks-to-5-for-first-time-in-2-1-2-years.html

Jul 1, 2013

The difference between the world’s two most-traded crude oil grades shrank to less than $5 a barrel for the first time in about 2 1/2 years, underlining the easing of a supply bottleneck in the U.S.

North Sea Brent crude’s premium to West Texas Intermediate narrowed to as little as $4.77 a barrel today. It’s the first time the spread between the two grades has been at $5 or less since Jan. 18, 2011, on an intraday basis, according to data compiled by Bloomberg. WTI, the main U.S. crude grade, had been typically the more expensive grade until mid-2010.

The drop in the gap between Brent, a gauge for more than half the world’s oil, and WTI shows how improved pipeline networks and the use of rail links have helped to unlock a glut at America’s oil-storage hub at Cushing, Oklahoma, in line with a prediction made by Goldman Sachs Group Inc. as long ago as February 2012. WTI rose 5.2 percent in the first half of this year. Brent dropped by 8.1 percent as North Sea supplies have stabilized following oilfield maintenance.

- more at link -

13

posted on

07/02/2013 2:40:08 AM PDT

by

thackney

(life is fragile, handle with prayer)

Disclaimer:

Opinions posted on Free Republic are those of the individual

posters and do not necessarily represent the opinion of Free Republic or its

management. All materials posted herein are protected by copyright law and the

exemption for fair use of copyrighted works.

FreeRepublic.com is powered by software copyright 2000-2008 John Robinson