Posted on 05/13/2017 8:20:06 AM PDT by Lorianne

Oh, and the unintended consequences of trying to regulate a monster. Economists at the New York Fed included this gem in their report on a two-day conference on “Derivatives and Regulatory Changes” since the Financial Crisis:

Though the notional amount [of derivatives] outstanding has declined in recent years, at more than $500 trillion outstanding, OTC derivatives remain an important asset class.

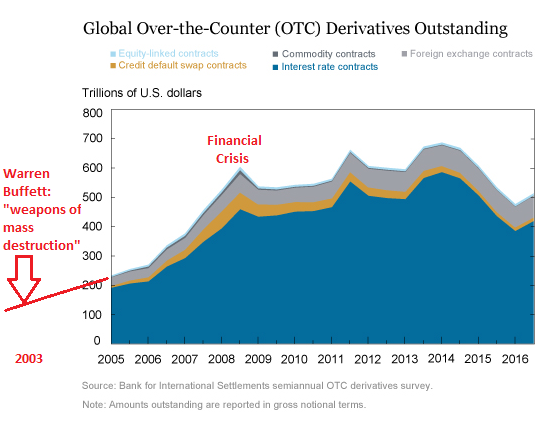

An important asset class. A hilarious understatement. Let’s see… the “notional amount” of $500 trillion is 25 times the GDP of the US and about 7 times global GDP. Derivatives are not just an “important asset class,” like bonds; they’re the largest “financial weapons of mass destruction,” as Warren Buffett called them in 2003.

Derivatives are used for hedging economic risks. And they’re used as “speculative directional exposures” – very risky one-sided bets. It’s all tied together in an immense and opaque market interwoven with the banks. The New York Fed:

The 2007-09 financial crisis highlighted weaknesses in the over-the-counter (OTC) derivatives markets and the increased risk of contagion due to the interconnectedness of market participants in these markets.

This chart from the New York Fed shows how derivatives ballooned 150% – or by $360 trillion – in less than four years before the Financial Crisis. They ticked down during the Financial Crisis, then rose again during the Fed’s QE to peak at $700 trillion. After the end of QE, they declined, but recently ticked up again to $500 trillion. I added in red the Warren Buffett moment:

The vast majority of the derivatives are interest rate and credit contracts (dark blue). Banks specialize in that. For example, according to the OCC’s Q4 2016 Report on Derivatives, JPMorgan Chase holds $47.5 trillion of derivatives at notional value and Citibank $43.9 trillion. The top 25 US banks hold $164.7 trillion, or 8.5 times US GDP. So even a minor squiggle could trigger some serious heartburn.

In 2003 already, famously, when there were less than $200 trillion in derivatives outstanding, Warren Buffett, who himself doesn’t shy away from them, warned in Berkshire Hathaway’s annual report:

I view derivatives as time bombs, both for the parties that deal in them and the economic system. Basically these instruments call for money to change hands at some future date, with the amount to be determined by one or more reference items, such as interest rates, stock prices, or currency values.Unless derivatives contracts are collateralized or guaranteed, their ultimate value also depends on the creditworthiness of the counter-parties to them.

But before a contract is settled, the counter-parties record profits and losses – often huge in amount – in their current earnings statements without so much as a penny changing hands. Reported earnings on derivatives are often wildly overstated. That’s because today’s earnings are in a significant way based on estimates whose inaccuracy may not be exposed for many years.

The errors usually reflect the human tendency to take an optimistic view of one’s commitments. But the parties to derivatives also have enormous incentives to cheat in accounting for them. Those who trade derivatives are usually paid, in whole or part, on “earnings” calculated by mark-to-market accounting. But often there is no real market, and “mark-to-model” is utilized. This substitution can bring on large-scale mischief.

As a general rule, contracts involving multiple reference items and distant settlement dates increase the opportunities for counter-parties to use fanciful assumptions. The two parties to the contract might well use differing models allowing both to show substantial profits for many years. In extreme cases, mark-to-model degenerates into what I would call mark-to-myth.

The derivatives genie is now well out of the bottle, and these instruments will almost certainly multiply in variety and number until some event makes their toxicity clear.

In my view, derivatives are financial weapons of mass destruction, carrying dangers that, while now latent, are potentially lethal.

That was in 2003. Five years later, it all came apart. Since the Financial Crisis, there have been some regulations globally to improve the functioning of OTC derivatives markets and manage “the risks associated with these products,” as the NY Fed’s report put it. But even today, there are still conferences on derivatives – for regulators to figure out how to regulate them, and for market participants to figure out how to get around these regulations. Hence “unintended consequences,” according to the New York Fed:

Some of the unintended consequences:

SNIP

Que the fiscally conthervative outrage at the fruits of their systemic moral corruption...

{ crickets crickets crickets }

The ‘notional value’ is meaningless. You have to look at the contract and see what the value at risk is.

Typically, derivatives contracts sold by banks to corporate customers are quite favorable to the bank, and unfavorable to the customer. On an interest-rate swap on a notional principal of $100 million, the customer might have to pay the bank $200,000 a month as long as the average 10-year Treasury is below 3%, and only be entitled to receive $150,000 a month if it goes above 3%. If the contract is for two years, the bank is highly likely to make money on the deal. In any case, the most they could lose on $100 million notional principal is $3.6 million, and that only if interest rates jump the week after the contract is signed. They are hedged even against this unlikely event.

They are a conjuring illusion. I.e. witchcraft.

>>look at the contract and see what the value at risk is.

LOL.

Who’s analyzing that?

How are these phantom “derivatives” classed as any sort of asset? They are deadly weight on the entire economy aand do not represent anything real or ultimately collectible.

Well said. A derivative is a contract.

I tell mom I will bring home some milk, and a pizza for my brother. Did I just increase the debt or money supply? Nope. And these agreements are not mutually exclusive.

I may renege, buy more or buy less.

Mom may promise Dad some milk, who promises a work buddy some milk. They created nothing new but promised trades.

Fraud is the problem though, when banks fractionally reserve their contracts and promise the same milk to multiple people. They should be hung.

Republicans, are you listening?

>>A derivative is a contract.

LOL.

Written on A$$Paper.

https://www.google.com/#q=asspaper+asset+backed+securities

>>Fraud is the problem though,

Look Closer.

(Right) https://www.google.com/#q=Roland+Arnall+George+Bush+Subprime

(Left) https://www.google.com/#q=Penny+Prizker+Obama+Subprime

Left Right Left Right... The sheeple getting marched down the dialectic Oligarchic Kleptocratic toilet!

...under the spreading derivative A.C.O.R.N. tree!

sounds like a horizontal ponzi scheme.

$500 trillion is just the notional amount. The actual liability is far less than that. The notional amount is just the hypothetical base amount on which the payments are calculated. You’re probably talking about a fraction of a percent of the notional amount. It’s still a big market but even that liability is contingent.

The value at risk is meaningless also ,, you’ll have a cascade effect where nothing does clear or can clear .. it’s all just an accounting gimmick to hedge and bolster reserves by making unsafe assets appear stable enough to be counted as reserves.

*******************

News about a very important asset class. Important because it facilitates fraud.

The banking/investment establishment, knowing all too well their own predilection toward expanding debt as a principal method of encouraging (haha) ‘prosperity’, embraced the expansion of derivative instruments quite literally from the date of the ebormous facilitation of derivatives trading, in this case ‘options’ on shares which occurred in 1973. Financial institutions, although a bit slow on the uptake, soon embraced this latest foray into expanded leverage and jumped in with both feet. One reason for this was what I call “automatic credit”, namely, the very act of trading an option creates perforce an increase in total market leverage.

Leverage, throughout all financial history, has been abused, usually to the point of, or past, collapse. How many examples would you like? (careful, pls, I can provide dozens).

In the 20th century, we saw the spectacular credit-fueled (i.e. levered) rise of the Dow averages in the 1920s and the widely celebrated (and HUGELY levered) rise of LTCM from 1994 through 1998. If you’re of a more historical turn of mind, just thumb through all the infamous ‘bubbles’ (tulips, South Sea, Mississippi land, check what you like).

‘Important’ asset class, eh? Well, I should hope to kiss a horse. THe problem occurs when (and in this case already has occurred) this ‘important’ asset class becomes the dominant asset class. Mae West put it well: “I can resist anything but temptation.”

More’s the pity, the same is true of the banking/investment class.

BTW, still haven’t heard from Pete. I **do** hope he’s well.

Best to you,

That “Important Investment Class” could very well blow up on us peons. I laughed at the labeling. What is your book about? My niece is going to start her on little trading company. ; )

Keeping my fingers crossed for your book.

I want to know why $100 buys far less.

Who is making out like a bandit?

Oligarchic Kleptocracy.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.