Posted on 01/08/2014 12:45:03 PM PST by thackney

Strong U.S. crude oil production growth forecast through 2015

Strong growth in U.S. crude oil production, primarily attributable to growing volumes of light crude oil produced from onshore tight oil formations, has reshaped global oil markets in recent years. EIA expects this growth trend to continue for the next two years, as forecast in this month's Short-Term Energy Outlook (STEO).

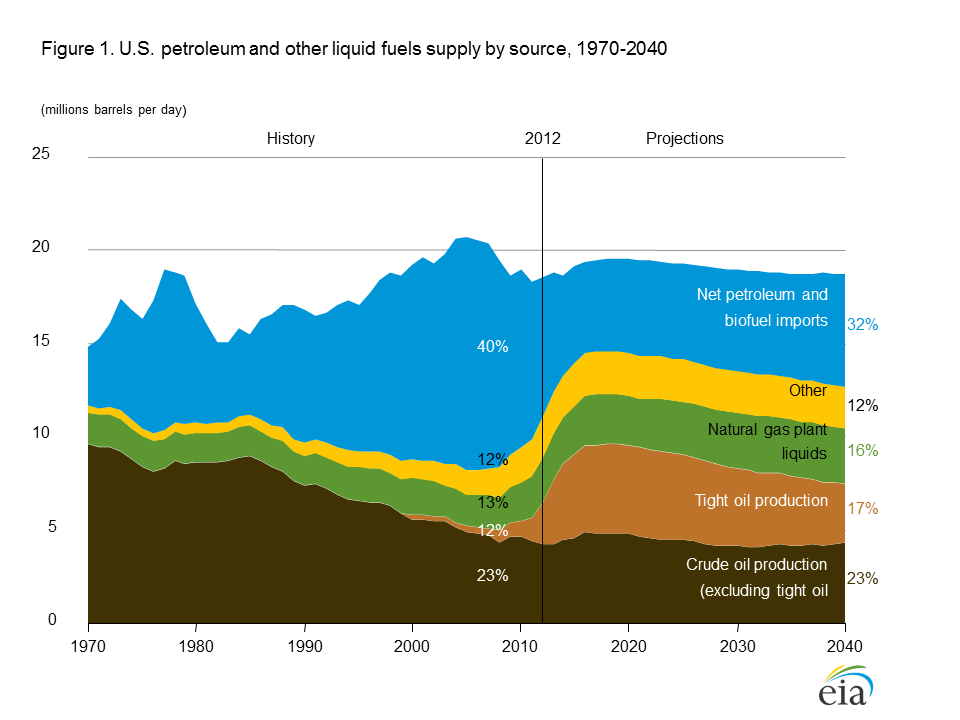

EIA estimates that U.S. crude oil production averaged 7.5 million barrels per day (bbl/d) in 2013, the highest annual average rate of production since 1989, and a 1.0-million-bbl/d increase from 2012 (Figure 1). In the January STEO, which extends the forecast period through 2015, EIA expects continued strong production growth. EIA projects crude oil production to average 8.5 million bbl/d in 2014 and 9.3 million bbl/d in 2015, which would be the highest annual rate of crude oil production since 1972. The record highest annual average crude oil production was 9.6 million bbl/d in 1970.

Production from tight oil formations in Texas, North Dakota, and a handful of other states has driven total crude oil production growth for the past four years. Development activity in these key onshore basins and increasing productivity as companies learn how to apply hydraulic fracturing techniques more effectively and efficiently are central to STEO's forecast. In particular, EIA expects most growth through 2015 to result from drilling in the Bakken formation in North Dakota and Montana, the Eagle Ford formation in Texas, and the Permian Basin in Texas and New Mexico. Bakken production is expected to rise from the estimated December 2013 level of 1.0 million bbl/d to 1.3 million bbl/d in December 2015. Eagle Ford production is projected to increase from an estimated December 2013 level of 1.2 million bbl/d to 1.5 million bbl/d in December 2015. The Eagle Ford accounts for more than half of the onshore domestic liquids production growth because of a comparatively large amount of liquids coming from both oil and gas wells compared with the other key production basins.

The Permian Basin in West Texas, which includes thick, overlapping formations such as the Spraberry, Bonespring, and Wolfcamp, is a third key growth area. EIA estimates that crude oil production from the Permian Basin reached 1.5 million bbl/d in December 2013 and is projected to increase to 1.8 million bbl/d in December 2015. Crude oil producers are investing heavily in research and implementation of hydraulic fracturing in both vertical and horizontal wells. The stacked formations of the Permian allow vertical wells to reach several productive zones, while several horizontal wells drilled from the same surface location can target different formations or several pay zones within the same formation.

While onshore crude oil production is expected to account for the bulk of the total production increase through 2015, projected growth also reflects expected increases in offshore production from the U.S. federal Gulf of Mexico (GOM). After offshore GOM oil production was flat at 1.3 million bbl/d in 2013, EIA projects GOM crude oil production will increase to 1.6 million bbl/d in 2015. The expected increases from GOM are the result of the following projects that are expected to come on stream: Jack, St. Malo, Entrada, Big Foot, Tubular Bells, Atlantis Phase 2 redevelopment, Hadrian South, and Lucius in 2014; Axe, Cardamom Deep, Dalmation, Deimos South, Kodiak, Pony, Samurai, West Boreas, Winter, and Mars B redevelopment in 2015.

These continuing increases in crude oil production are having profound effects on U.S. petroleum balances and global oil prices. EIA expects the discount of the WTI crude oil price to Brent to average $12 per barrel (bbl) in 2014, $3/bbl higher than projected in last month's STEO. This increase in the projected WTI discount reflects increasing uncertainty about existing refinery infrastructure's ability to absorb growing production of light sweet crude oil in North America at current price levels. Because of pipeline capacity expansions and pipeline reversals, there is now ample capacity to ship crude oil via pipeline from the previous bottleneck in the Midcontinent to the Gulf Coast. As a result, Light Louisiana Sweet (LLS) crude oil on the Gulf Coast, which was priced at a premium to North Sea Brent for much of the past two years, has recently begun tracking WTI prices and selling at a consistent discount to Brent. Thus, EIA expects the recent convergence of Gulf Coast crude oil prices with WTI to persist over the forecast period, with Gulf Coast crude oil prices moving in step with the WTI price plus a pipeline transport cost. At this price level, Gulf Coast crudes such as LLS and medium-grade Mars will trade at historically wide discounts to similar international benchmarks such as Brent and Dubai, respectively. The forecast relationship between Brent, WTI, and LLS prices in 2015 are similar to those expected in 2014.

Gasoline price flat while diesel fuel up slightly

The U.S. average retail price of regular gasoline increased less than one cent to remain at $3.33 per gallon as of January 6, 2014, three cents higher than last year at this time. Prices increased in all regions of the nation except the Midwest, where the price declined four cents to $3.22 per gallon. The largest increase came on the East Coast, where the price was up three cents to $3.44 per gallon. Both the Rocky Mountain and West Coast prices gained two cents, to $3.12 per gallon and $3.55 per gallon, respectively, and the Gulf Coast price was $3.12 per gallon, a penny higher than last week.

The national average diesel fuel price increased one cent to $3.91 per gallon, less than a penny lower than last year at this time. Prices increased in all regions of the nation, with the East Coast, Gulf Coast, and Rocky Mountain prices all gaining one cent, to $3.95 per gallon, $3.80 per gallon, and $3.90 per gallon, respectively. The West Coast average rose nearly a cent, but remained at $4.03 per gallon, while the Midwest price increased only fractionally, and remained at $3.89 per gallon.

Propane inventories fall

U.S. propane stocks fell by 3.5 million barrels to end at 42.4 million barrels last week, 23.1 million barrels (35.3%) lower than a year ago. Gulf Coast regional inventories dropped by 2.1 million barrels and Midwest inventories decreased by 1.2 million barrels. Rocky Mountain/West Coast and East Coast inventories both dropped by less than 0.1 million barrels. Propylene non-fuel-use inventories represented 8.5% of total propane inventories.

Residential propane price continues to increase, heating oil price decreases Residential heating oil prices decreased by nearly 2 cents per gallon to reach a price of $4.02 per gallon during the period ending January 6, 2014. This is less than 2 cents per gallon higher than last year's price at this time. Wholesale heating oil prices decreased 15 cents per gallon last week to $3.07 per gallon.

The average residential propane price increased by almost 3 cents per gallon last week to nearly $2.83 per gallon, 56 cents per gallon higher than the same period last year. Wholesale propane prices decreased by less than a penny per gallon to just under $1.69 per gallon as of January 6, 2014.

6.5 million barrels per day (bbl/d) in 2012

7.5 million barrels per day (bbl/d) in 2013

8.5 million barrels per day (bbl/d) in 2014

9.3 million barrels per day (bbl/d) in 2015

Higher than I would have thought sustainable. But more in line with your projections.

Despite the best efforts of the regime, energy production continues to roll. Very ironic.

I’m a bit surprised at the ethanol production rising, here in Indiana a bunch of the new plants that sprung up in mid 2000s have closed up. The ones left must take up the slack.

SHORT-TERM ENERGY OUTLOOK

http://www.eia.gov/forecasts/steo/

Highlights

After falling to the lowest monthly average of 2013 in November, U.S. regular gasoline retail prices increased slightly to reach an average of $3.28 per gallon (gal) during December. The annual average regular gasoline retail price, which was $3.51/gal in 2013, is expected to fall to $3.46/gal in 2014 and $3.39/gal in 2015.

The North Sea Brent crude oil spot price in December averaged near $110 per barrel (bbl) for the sixth consecutive month. EIA expects the Brent crude oil price to decline gradually to average $105/bbl and $102/bbl in 2014 and 2015, respectively. Projected West Texas Intermediate (WTI) crude oil prices average $93/bbl during 2014 and $90/bbl during 2015.

EIA expects liquid fuels production from countries outside of the Organization of the Petroleum Exporting Countries (OPEC) to grow year-over-year by a record high of 1.9 million barrels per day (bbl/d) in 2014. The United States and Canada together are projected to account for almost 70% of total non-OPEC supply growth this year.

EIA estimates U.S. total crude oil production averaged 7.5 million bbl/d in 2013, an increase of 1.0 million bbl/d from the previous year. Projected domestic crude oil production continues to increase to 8.5 million bbl/d in 2014 and 9.3 million bbl/d in 2015. The 2015 forecast would mark the highest annual average level of production since 1972.

Natural gas working inventories on December 27 totaled 2.97 trillion cubic feet (Tcf), 0.56 Tcf below the level at the same time a year ago and 0.29 Tcf below the previous five-year average (2008-12). EIA expects that the Henry Hub natural gas spot price, which averaged $3.73 per million British thermal units (MMBtu) in 2013, will average $3.89/MMBtu in 2014 and $4.11/MMBtu in 2015.

Coal production, which fell by almost 9% between 2011 and 2013, is expected to increase by 36 million short tons (MMst) (3.6%) in 2014 as higher natural gas prices favor the dispatch of coal-fired power plants and the drawdown of coal inventory ends. In 2015, however, forecast coal-fired production falls by 2.5% with declining coal use in the electric power sector as retirements of coal-fired power plants rise due to the implementation of the U.S. Environmental Protection Agency’s Mercury and Air Toxics Standards.

Yep, and that’s why the Saudis are freaking out.

I don’t think $90~95/bbl is going to really hurt them.

With a growing industry like this working against the grain of the government I can imagine what our economic outlook would do under a pro business government.

B0 Soetoro and congress will claim credit here politically, while trying to explain to their Saudi masters how they messed up.

How do you think these price levels would affect exploration and development budgets for U.S. onshore tight oil formations?

The Energy Information Administration is predicting both in the same report.

So their expectation is that the US production will grow 1 MMBPD at $93/bbl in 2014 and grown another 0.8 MMBPD at $90/bbl in 2015.

I was looking for your take on the impact of these crude prices on oil companies' exploration and development budgets for tight oil formations. Do you have a sense for that?

Projections in the Annual Energy Outlook 2014

http://www.eia.gov/forecasts/aeo/er/executive_summary.cfm

The mystery to me is why they just said that production would peak and flatten out at the end of 2015.

I figure that eagle ford and the baaken should slow down considerably their gains—which would account for the flattening.however the 1000 foot deep plays in the permian are so great and so accessible and so untouched that you would think the permians yearly growth rate would just explode going out two years from now.

right now most of the permian basin oil is got from vertical wells. they’re only just starting to do the horizontal fracking and the multiwell pads and all the new stuff. You would think that two years from now they’d have the manufacturing mastered and the permian would be adding a half million or more barrels a day annually. Its just that big. What is the size of the addressable oil in the permian? 10 times the size of baaken and eagle ford combined? when the fracked oil from there get moving its going to come a gusher.

And it won’t be so expensive either. so even oil at $80@ barrel won’t discourage production—like it will in the baaken.

because that has to be the case and because the eia has raised their estimates every 6 months, I think it reasonable to say that 2016-2018 will also see near million barrel@ day production increases.

Wait a minute. Say the permian is adding 500k barrels @ day additional production. Where is the other 500k coming from? The gulf is going to add another 150k barrels @ day in 2016. The Oklahoma oil production is going straight up from fields they’re just getting into. They’ll be add 150k@day oil production.

Colorado oil production is also going straight up. They’ll be up around 100k@day oil production increases by 2016. That leaves 100k@ day from various other fields around the country or not.

but you get the picture.

Tubular Bells???

Show me the person who named that project, and I'll show you the person who has all the Exorcist movies.

The horizontal wells were to increase well bore contact with thin layers. If you have a very thick layer, the economic differential payout of a horizontal bore is diminished.

Thickness is not equal to “richness”.

In the Permian, the new production per rig continues to decline slightly.

http://www.eia.gov/petroleum/drilling/pdf/permian.pdf

Now compare that to the Eagle Ford.

http://www.eia.gov/petroleum/drilling/pdf/eagleford.pdf

The horizontal wells were to increase well bore contact with thin layers. If you have a very thick layer, the economic differential payout of a horizontal bore is diminished.

...........

I’m not getting that. I can see that production per well is flat in the permian. and total rig count is declining. I still don’t understand why. I thought it was just because they have not even started to do horizontal drilling. that its mostly been vertical drilling.

but judging by the graphs there’s some other issue involved. I don’t get it. How can you have an oil field like the permian with 10 times the addressable oil of baaken and eagle ford with multiple layers stacked one on top of the other. so that one drilling pad can do 30+ wells at different levels and directions...and the production per well be flat to down. and total production barely be up at all.

There’s something here I don’t understand.

The answer to my exploration budget question may lie in breakeven estimates here. Their breakeven estimates for unconventional oil plays, by basin, as of early last month: Eagle Ford $65, Bakken Core $75, Permian $80, Niobrara $80, Bakken Fringe $85, Utica $85, Mississippian $85,Cana Woodford $90, Ardmore Woodford $95

.............

this is very helpful info. I would have thought that the permian would be cheaper because there’s so much of it so densely packed. but I guess not. I wonder why they’re even drilling in the woodford. it has to be that with practice they figure they can get costs down. For example I’ve read that continental in the baaken has got their costs down to $60@ barrel—or $15 under 75. Continental is shifting serious resources over to the cana woodford.

Thanks thackney.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.